Bill Gross Ponders "Deep Demographic Doo-Doo"

Economics / Demographics Jul 29, 2010 - 03:46 AM GMTBy: Mike_Shedlock

Bill Gross usually writes an interesting column provided you skip over the first few paragraphs of introduction. His August Investment Outlook regarding population demographics is no different. Please consider Private Eyes.

Bill Gross usually writes an interesting column provided you skip over the first few paragraphs of introduction. His August Investment Outlook regarding population demographics is no different. Please consider Private Eyes.

Our modern era of capitalism over the past several centuries has never known a period of time in which population declined or grew less than 1% a year. Currently, the globe is adding over 77 million people a year at a pace of 1.15% annually, but slowing.

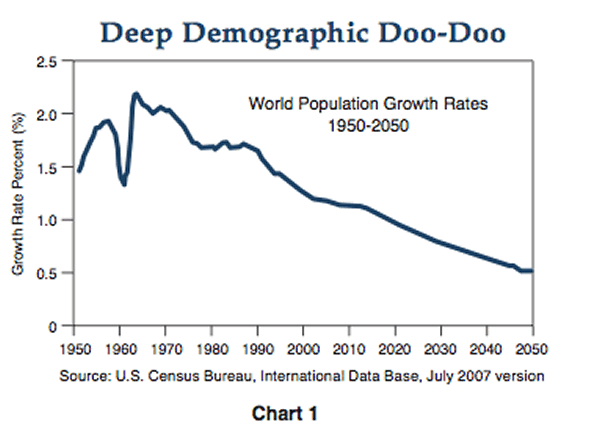

Observers will point out, as shown in the following chart, that global population growth rates have been declining since 1970 with no apparent ill effects. True, until 2008, I suppose. The fact is that since the 1970s we have never really experienced a secular period during which the private market could effectively run on its own engine without artificial asset price stimulation. The lack of population growth was likely a significant factor in the leveraging of the developed world’s financial systems and the ballooning of total government and private debt as a percentage of GDP from 150% to over 300% in the United States, for example. Lacking an accelerating population base, all developed countries promoted the financing of more and more consumption per capita in order to maintain existing GDP growth rates. Finally, in the U.S., with consumption at 70% of GDP and a household sector deeply in debt, there was nowhere to go but down. Similar conditions exist in most developed economies.

The danger today, as opposed to prior deleveraging cycles, is that the deleveraging is being attempted into the headwinds of a structural demographic downwave as opposed to a decade of substantial population growth. Japan is the modern-day example of what deleveraging in the face of a slowing and now negatively growing population can do.

The preceding analysis does not even begin to discuss the aging of this slower-growing population base itself. Japan, Germany, Italy and of course the United States, with its boomers moving toward their 60s, are getting older year after year. Even China with their previous one baby policy faces a similar demographic. And while older people spend a larger percentage of their income – that is, they save less and eventually dissave – the fact is that they spend far fewer dollars per capita than their younger counterparts. No new homes, fewer vacations, less emphasis on conspicuous consumption and no new cars every few years. Healthcare is their primary concern. These aging trends present a one-two negative punch to our New Normal thesis over the next 5–10 years: fewer new consumers in terms of total population, and a growing number of older ones who don’t spend as much money. The combined effect will slow economic growth more than otherwise.

PIMCO’s continuing New Normal thesis of deleveraging, reregulation and deglobalization produces structural headwinds that lead to lower economic growth as well as half-sized asset returns when compared to historical averages. The New Normal will not be aided nor abetted by a slower-growing population nor by cyclical policy errors that thrust Keynesian consumption remedies on a declining consumer base. Current deficit spending that seeks to maintain an artificially high percentage of consumer spending can be compared to flushing money down an economic toilet.

Keynesian Stimulus is Money Flushed Down the Toilet

Please read that last paragraph closely. Here is the key sentence "The New Normal will not be aided nor abetted by a slower-growing population nor by cyclical policy errors that thrust Keynesian consumption remedies on a declining consumer base."

If anyone needs to read that paragraph, it is none other than PIMCO's Paul McCulley.

Flashback Sunday, January 10, 2010: Pimco's Paul McCulley Wants Japan To Go "All In"

In spite of the complete failure of Keynesian and Monetarist policies of Japan over two decades, amazingly Paul McCulley wants Japan to go "All In".

“Japan’s problem is deflation, not inflation as far as an eye can see,” wrote Paul McCulley, a member of the investment committee, and Tomoya Masanao, the head of portfolio management for Japan, in a report on the Web site of Newport Beach, California-based Pimco. “An ‘all-in’ reflationary policy is what is needed.”

The BOJ may also consider promising to refrain from raising interest rates until inflation becomes “meaningfully positive,” McCulley and Masanao said.

Definitions of Insanity

- In One Sentence: Insanity is doing the same thing over and over and over and expecting different results each time.

- In Two Words: Paul McCulley

- In One Word: Keynesianism

- In Another Word: Monetarism

Japan has already gone "all in". It has tried everything under the sun for two decades including Keynesianism, Monetarism, and selling its own currency to sink it. All it has to show for its efforts is a massive pile of debt equaling 227% of GDP.

Amazingly, some people have learned nothing from two decades of complete failure.Send a Message to McCulley

I am glad to see Bill Gross admit that McCully advocates "flushing money down an economic toilet" because that is exactly what McCully has proposed on numerous occasions. My question now is "How long it will take for Gross to relay the message to McCulley?"

Now, if we can only get the message to Obama, Geithner, Krugman, Barney Frank, Nancy Pelosi, and all the other Keynesian clowns perhaps it would do some good.

That said, I do have one point of contention with Gross: Demographics or not, Keynesian stimulus never works. The idea one can spend one's way to prosperity is preposterous. As Japan has proven, attempts to do so in tantamount to a can-kicking escapade at best, and an unsustainable Ponzi scheme at worst. I lean towards the latter.

Not once do any of the Keynesian clowns ever address the question "What happens when the stimulus runs out?"

Keynesian Definition of Temporary is Forever

Take note of the $8,000 housing tax credits. Demand picked up and then subsequently collapsed. What next? Do we buy everyone a house whether they need one or not?

That is essentially what McCulley suggested when he asked for Japan to go "All In". That is what Krugman and others are suggesting still.

Geithner portrays it as "temporary".

The Keynesian definition of temporary is "until it works". In other words "forever" because lunacy cannot and will not work in a sustainable fashion. It only appears to work for short-term durations.

The classic example is the Greenspan induced housing bubble. Unemployment dropped to record lows , GDP soared, but in the end the bubble collapsed.

That is what "All In" does.

Demographic Analysis

While I commend the viewpoint of Bill Gross, it is hardly revolutionary except perhaps of his implied criticism of McCulley.

Thursday, May 01, 2008: Demographics Of Jobless ClaimsStructural Demographics Poor

Structural demographic effects imply that prospects in the full-time labor market will be poor for those over age 50-55 and workers under age 30. Teen and college-age employment could suffer a great deal from (1) a dramatic slowdown in discretionary spending and (2) part-time Boomer reentrants into the low-paying service sector; workers who will be competing with younger workers.

Ironically, older part-time workers remaining in or reentering the labor force will be cheaper to hire in many cases than younger workers. The reason is Boomers 65 and older will be covered by Medicare (as long as it lasts) and will not require as many benefits as will younger workers, especially those with families. In effect, Boomers will be competing with their children and grandchildren for jobs that in many cases do not pay living wages.

Consider what such a decline in US GDP growth and its multiplier effect could mean for Asian growth, global trade, demand for commodities, and growth elsewhere in the world (BRIC).

The world equities markets have barely begun to discount the increasingly likely severe deceleration in US and world GDP growth ahead, including the secular Boomer drawdown of accumulated wealth of the past 25 yrs.Monday, August 31, 2009: Spending Collapses In All Generation Groups

Boomer Statistics

Those stats are from a McKinsey study, and there is nothing remotely inflationary about boomer demographics.

- $400 Billion: Amount that will come out of annual U.S. consumption as thrifty boomers push savings rate from 1% to nearly 5%.

- 47%: Boomers share of national disposable income in 2005 before the bubble burst. Boomers contributed only 7% to national savings.

- 2.4%: Forecasted GDP growth over the next three decades as boomers ratchet back. GDP has grown 3.2% a year since 1965.

- 69%: Portion of boomers aged 54 to 63 who are financially unprepared for retirement.

- 78%: Boomers' share of GDP growth during the bubble years of 1995 to 2005

Nor is there anything inflationary about Generation X demographics. Generation X's have seen boomers blow it. By sharply curtailing spending, generation X at least has chance to right the ship before retirement. It's too late for most boomers. Time ran out.

Now consider generation Y with 19% of the population. Think the income levels of generation Y are going to catch boomers or generation X?

When?

Finally, think about tightening lending standards and attitudes about debt in general. Because of lower incomes and tighter lending standards, it is unlikely that Generation Y will be either able or willing to carry debt burdens to sustain a strong recovery.

Distortionary vs. Inflationary

Bernanke can flood the world with "reserves" and indeed he has. However, he cannot force banks to lend or consumers to borrow.

Here is a simple analogy that everyone should be able to understand: You can lead a horse to water but you cannot make it drink. And if the horse does not want to drink, it was a waste of time and energy to lead the horse to the water.

Yet every day someone comes up with another convoluted theory about how inflationary this all is. It is certainly "distortionary" in that it creates problems down the road and prolongs a real recovery by keeping zombie banks alive (as happened in Japan). However, it is not (in aggregate) going to cause massive inflation because it is not spurring the creation of new debt.

Recognition Phase

I have been talking about these trends for quite some time. The fact that Bill Gross is discussing these trends now is part of the "Recognition Phase".

Bear in mind that Robert Prechter figured this out decades ago, far before most anyone else, indeed far too soon to do him or anyone else any good. Consumers figured it out a year ago. Mainstream media of which Bill Gross is an early practitioner is just starting to catch on. Bill Gross is behind bloggers, but he is far ahead of most of his peers.

By the time mainstream media fully embraces these trends we will be two thirds through it. Such is the nature of the game.

Brutal Combination

Please note that it is not demographics per se that is doing us in, but rather enormous amounts of consumer debt (as a result of decades of Keynesian and Monetarist stimulus) in conjunction with unfavorable demographics and global wage arbitrage that is doing us in. Bill Gross missed this essential point.

By Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management . Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction.

Visit Sitka Pacific's Account Management Page to learn more about wealth management and capital preservation strategies of Sitka Pacific.

I do weekly podcasts every Thursday on HoweStreet and a brief 7 minute segment on Saturday on CKNW AM 980 in Vancouver.

When not writing about stocks or the economy I spends a great deal of time on photography and in the garden. I have over 80 magazine and book cover credits. Some of my Wisconsin and gardening images can be seen at MichaelShedlock.com .

© 2010 Mike Shedlock, All Rights Reserved.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.