Peacock Syndrome – America’s Fatal Disease

Politics / US Debt Jul 24, 2011 - 07:14 PM GMTBy: James_Quinn

"There will be, in the next generation or so, a pharmacological method of making people love their servitude, and producing dictatorship without tears, so to speak, producing a kind of painless concentration camp for entire societies, so that people will in fact have their liberties taken away from them, but will rather enjoy it, because they will be distracted from any desire to rebel by propaganda or brainwashing, or brainwashing enhanced by pharmacological methods. And this seems to be the final revolution." - Aldous Huxley

"There will be, in the next generation or so, a pharmacological method of making people love their servitude, and producing dictatorship without tears, so to speak, producing a kind of painless concentration camp for entire societies, so that people will in fact have their liberties taken away from them, but will rather enjoy it, because they will be distracted from any desire to rebel by propaganda or brainwashing, or brainwashing enhanced by pharmacological methods. And this seems to be the final revolution." - Aldous Huxley

Researchers at the University of Texas recently published a study about why men buy or lease flashy, extravagant, expensive cars like a gold plated Porsche Carrera GT. There conclusion was:

"Although showy spending is often perceived as wasteful, frivolous and even narcissistic, an evolutionary perspective suggests that blatant displays of resources may serve an important function, namely as a communication strategy designed to gain reproductive rewards."

To put that in laymen's terms, guys drive flashy expensive cars so they can get laid. Researcher Dr Vladas Griskevicius said: "The studies show that some men are like peacocks. They’re the ones driving the bright colored sports car."

Lead author Dr Jill Sundie said: "This research suggests that conspicuous products, such as Porsches, can serve the same function for some men that large and brilliant feathers serve for peacocks." The male urge to merge with hot women led them to make fiscally irresponsible short term focused decisions. I think the researchers needed to broaden the scope of their study. Millions of Americans, men and women inclusive, have been infected with Peacock Syndrome. Millions of delusional Americans thought owning flashy things, living in the biggest McMansion, and driving a higher series BMW made them more attractive, more successful, and the most dazzling peacock in the zoo.

This is not a attribute specific to Americans, but a failing of all humans throughout history. Charles Mackay captured this human impulse in his 1841 book Extraordinary Popular Delusions and the Madness of Crowds:

“Men, it has been well said, think in herds; it will be seen that they go mad in herds, while they only recover their senses slowly, and one by one.”

The herd has been mad since 1970 and with the post economic collapse of 2008, some people are recovering their senses slowly, and one by one. The country was overrun by flocks of ostentatious peacocks displaying their plumage in an effort to impress their friends, families and work colleagues. What set the flaunting American peacocks apart was the fact they financed their splendid display of plumage with $0 down and 0% interest for seven years. The lifestyles of the rich and famous miraculously became available to the poor and middle class through the availability of easy abundant credit provided by the friendly kind hearted Wall Street banks and their heroin dealers at the Federal Reserve.

The United States has experienced a four decade long “expenditure cascade”. An expenditure cascade occurs when the rapid income growth of top earners fuels additional spending by the lower earner wannabes. The cascade begins among top earners, which encourages the middle class to spend more which, in turn, encourages the lower class to spend more. Ultimately, these expenditure cascades reduce the amount that each family saves, as there is less money available to save due to extra spending on frivolous discretionary items. Expenditure cascades are triggered by consumption. The consumption of the wealthy triggers increased spending in the class directly below them and the chain continues down to the bottom. This is a dangerous reaction for those at the bottom who have little disposable income originally and even less after they attempt to keep up with others spending habits.

This cascade of expenditures could not have occurred without cheap easy credit, supplied by Wall Street shysters and abetted by their puppets at the Federal Reserve through their inflationary policies. Real wages are lower today than they were in 1970. Coincidentally, the credit card began its ascendance as the peacock payment of choice in 1970. There are now over 600 million credit cards in circulation in the U.S. in the hands of 177 million fully plumed peacocks and peacock wannabes.

Monthly Payment Nation

“Consumerism requires the services of expert salesmen versed in all the arts (including the more insidious arts) of persuasion. Under a free enterprise system commercial propaganda by any and every means is absolutely indispensable. But the indispensable is not necessarily the desirable. What is demonstrably good in the sphere of economics may be far from good for men and women as voters or even as human beings.” - Aldous Huxley

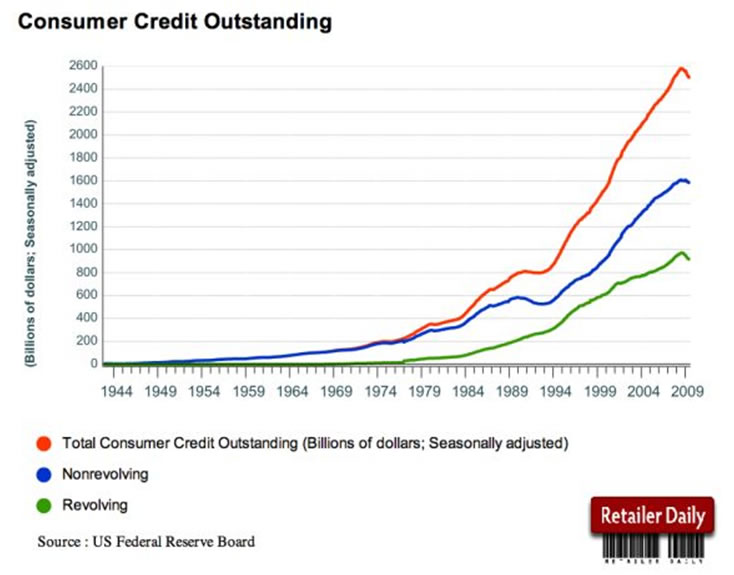

The country seemed to do just fine from 1945 through 1970 with no credit card debt and moderate levels of auto loan debt. In fact, this period in U.S. history was marked by strong economic growth created by capital investment, savings, and the American middle class realizing the American dream of a better life based upon their work ethic. Around about 1970, the intersection of Baby Boomers coming of age, the belief that social justice for all was a noble goal, and Nixon’s closing the gold window, opened Pandora’s Box and the evil released has brought the country to the precipice of ruin. Today, consumer credit outstanding totals $2.43 trillion, or $22,000 per household. It peaked at $2.6 trillion in 2008 and the storyline fed to the masses was that Americans had seen the light and embraced frugality by paying off their debts. As with most storylines spouted by the mainstream media, it was completely false. The Wall Street banks wrote off over $200 billion since 2008, while delusional peacocks continued to finance and lease gas guzzling luxury automobiles, while charging their purchase of an iPad2 and Lady Gaga concert tickets on one of their 13 credit cards.

It seems a vast swath of America refuse to shed their peacock feathers. This explains why you see BMWs, Mercedes, Escalades, and Porsches parked in the driveways of $100,000 houses. Automobiles are the truest representation of American peacock syndrome. Very few people look at a car purchase in a rational long term financial sense. It’s about impressing the neighbors, your peers and your family. Driving a brand new luxury car gives you the appearance of success. The neighbors don’t know you are in debt up to your eyeballs. This explains why 30% to 40% of all luxury cars are leased. A man could buy a $20,000 Honda hybrid with 10% down and finance the rest at 0.9% for three years. His monthly payment would be $500. After three years he would own the car outright, with the added benefit of getting 45 mpg. He could then invest the $500 per month for the next seven years in gold and silver or something else that benefits from Federal Reserve created inflation. In today’s society this would be the act of a doo doo bird.

Why drive a putt putt car when you can drive the ultimate peacock machine – a BMW 528i with 24-valve inline 240-horsepower 6-cylinder engine with composite magnesium/aluminum engine block, Valvetronic, and Double-VANOS steplessly variable valve timing, 10-way power-adjustable driver's and front passenger's seat with 4-way lumbar support, and memory system for driver's seat, steering wheel and outside mirrors, along with high-fidelity 12-speaker sound system, including 2 subwoofers under the front seats, and digital 7-channel amplifier with 205 watts of power. Plus it looks really cool. This materialism machine can be leased for the same $500 per month that the doo doo bird pays for his Honda hybrid. Of course, after three years of renting luxury wheels the peacock has to turn in the 528i and lease an equally luxurious auto because driving an economy car would now harm his reputation. Colorful plumage is everything to a peacock.

Sometime over the years Americans lost their bearings and began to ignore a basic truth. The only way to accumulate wealth is to spend less than you make and save the difference. Over a ten year time frame the peacock will have dished out $60,000 renting luxury cars, while the doo doo bird will have expended $21,000 during the first three years and then invested $500 per month for 84 months, leaving him with a net $25,000 asset, based on a modest investment return of 5%. The doo doo bird ends up $85,000 wealthier than the peacock at the end of ten years. If you peruse the car dealer advertisements in your local paper, the price of the car is rarely even printed, only the monthly lease payment or 0% financing offer. There is a reason why the average American lives paycheck to paycheck, has no emergency fund for a rainy day, and has virtually no retirement savings socked away. Status, reputation and the appearance of success became more important to millions of Americans than living within their means and actually sacrificing and doing the hard work required to succeed. Delayed gratification is an unknown concept in America.

In 1970, 37% of households consisted of 4 or more people and we somehow managed to get by with one four door car per household. Today, only 24% of households consist of 4 or more people. There are 113 million households and over 250 million passenger vehicles, or 2.2 per household. So, even though the number of people in our households has shrunk dramatically, we needed 120% more vehicles to transport our vast quantities of stuff. Not only do we have more vehicles, but the size of these symbols of gluttony has doubled and tripled, with fitting names like: Tundra, Navigator, Titan, Yukon, Suburban and Hummer. Every soccer mom with two kids needed a 20 foot long, 6 foot high Yukon with an 8 cylinder engine, getting 12 mpg to shuttle around little Aiden and Chloe to their ten scheduled weekly activities. It wasn’t only automobiles that Americans went gaga over. The average home size in 1970 was 1,400 square feet (we drive cars bigger than that today). By 2009, the average home size reached 2,700 square feet. God knows we need 12 rooms for our 2.4 person households. The expenditure cascade started as a trickle in 1970 but became a raging uncontrollable waterfall by 2008.

Delusional Americans have been slowly lured into the web of debt and living their lives based upon whether they can make the monthly payment on their debt. I can anticipate the outrage from those who declare it wasn’t them, it was the other guy. Everyone has an excuse for why they aren’t to blame, but the facts speak otherwise:

- Non-revolving (auto & education) debt outstanding is at an all-time high of $1.64 trillion.

- The average auto loan is now $27,000 with a loan to value ratio of 80% to 90%, down from 95% in 2007.

- Auto dealers are now offering $0 down and 0% interest for 72 months on many models. Ask yourself how a finance company can make a profit with those terms.

- There are 54 million households with a revolving credit card balance, proving that approximately 50% of Americans are attempting to live above their means.

- The average credit card debt per household with credit card debt is $14,687.

- The average APR on a new credit card is 15%, even though the banks can borrow from the Federal Reserve for 0.25%.

- In 2009, the United States Census Bureau determined there were nearly 1.5 billion credit cards in use in the U.S. A stack of all those credit cards would reach more than 70 miles into space -- and be almost as tall as 13 Mount Everests.

- 76% of undergraduates have credit cards, and the average undergrad has $2,200 in credit card debt. Additionally, they will amass almost $20,000 in student debt.

- On average, today's consumer has a total of 13 credit obligations on record at a credit bureau. These include credit cards (such as department store charge cards, gas cards, and bank cards) and installment loans (auto loans, mortgage loans, student loans, etc.).

- Over 90 percent of African-American families earning between $10,000 and $24,999 had credit card debt. What bank in their right mind would issue a credit card to someone making $15,000 per year?

- Discussing credit card debt is highly taboo. The topics at the top of the list of things that people say they are very or somewhat unlikely to talk openly about with someone they just met were: The amount of credit card debt (81%); details of your love life (81%); your salary (77%); the amount you pay for your monthly mortgage or rent (72%); your health problems (62%); your weight (50%). I wonder why?

- Penalty fees from credit cards added up to about $20.5 billion in 2009, according to R. K. Hammer, a consultant to the credit card industry. Don’t be one day late with that credit card payment. It’s good to be a bank.

- The average late fee was found to have risen to $28.19, way up from $25.90 in 2008. Consumer Action reported that late fees reached up to $39 per incident.

- The volume of gasoline purchases placed on credit cards jumped 39% last month from a year earlier, compared with a 21% increase in June 2010. Food shopping increased 5% after falling 7% last year. The value of an average transaction on credit cards outpaced the gain for debit cards, showing consumers are increasingly relying on borrowing to pay for gasoline and other necessities.

After decades of a debt financed contest to display the gaudiest plumage, is the average American happier? Considering more than 10% of all Americans are on anti-depressant drugs, I’d say not. The rat race for status, the appearance of wealth and visible faux displays of success do not increase well-being. If most of our earnings are spent on an empty game of status, we should not expect much improvement in our quality of life. There is something perverse about having more than enough. When we have more, it is never enough. It is always somewhere out there, just out of reach. This is the attitude that drives the criminals on Wall Street and politicians in Washington DC to constantly seek more power and wealth. The more we acquire, the more elusive enough becomes. Much of the debt financed purchases of consumer trinkets, baubles and gadgets is nothing more than an expensive anesthetic to deaden the pain of empty lives.

Based upon the facts, the average American has not benefitted from the decades long materialistic frenzy. They have sacrificed their futures for the fleeting glory of ephemeral riches. In fact, the average American could not have participated in the expenditure cascade had they not been enabled by the financial industry and cheap plentiful money provided by the financial industries’ drug dealer – the Federal Reserve. The financial industry complex used their power and wealth to utilize all means of propaganda and mass media outlets to convince Americans that debt was good and more debt was even better. I’ll address the insidious aspects of the unholy union of debt and propaganda in Part Two – Propaganda Nation Built Upon Delusions of Debt.

Meanwhile, millions of Americans cling to their borrowed peacock feathers as the butcher of reality bears down upon them. The end won’t be pretty. The brave conquerors of strip malls across the land can enjoy their toys, gadgets, and treasures for awhile longer, but they need to remember one thing - Glory is fleeting and death can come suddenly.

"For over a thousand years Roman conquerors returning from the wars enjoyed the honor of triumph, a tumultuous parade. In the procession came trumpeteers, musicians and strange animals from conquered territories, together with carts laden with treasure and captured armaments. The conquerors rode in a triumphal chariot, the dazed prisoners walking in chains before him. Sometimes his children robed in white stood with him in the chariot or rode the trace horses. A slave stood behind the conqueror holding a golden crown and whispering in his ear a warning: that all glory is fleeting."

Patton

Join me at www.TheBurningPlatform.com to discuss truth and the future of our country.

By James Quinn

James Quinn is a senior director of strategic planning for a major university. James has held financial positions with a retailer, homebuilder and university in his 22-year career. Those positions included treasurer, controller, and head of strategic planning. He is married with three boys and is writing these articles because he cares about their future. He earned a BS in accounting from Drexel University and an MBA from Villanova University. He is a certified public accountant and a certified cash manager.

These articles reflect the personal views of James Quinn. They do not necessarily represent the views of his employer, and are not sponsored or endorsed by his employer.

© 2011 Copyright James Quinn - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

James Quinn Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.