Assessing the Damage of the European Banking Crisis

Interest-Rates / Credit Crisis 2011 Oct 24, 2011 - 01:39 AM GMTBy: STRATFOR

Europe faces a banking crisis it has not wanted to admit even exists.

Europe faces a banking crisis it has not wanted to admit even exists.

The formal authority on financial stability, International Monetary Fund (IMF) chief Christine Lagarde, made her institution’s opinion on European banking known back in August when she prompted the European Union to engage in an immediate 200 billion-euro bank recapitalization effort. The response was broad-based derision from Europeans at the local, national and EU bureaucratic levels. The vehemence directed at Lagarde was particularly notable as Lagarde is certainly in a position to know what she was talking about: Until July 5, her title was not IMF chief, but French finance minister. She has seen the books, and the books are bad. Due to European inaction, the IMF on Oct. 18 raised its estimate for recapitalization needs from 200 billion euros to 300 billion euros ($274 billion to $410 billion).

Sovereign Debt: The Expected Problem

The collapse in early October of Franco-Belgian bank Dexia, a large Northern European institution whose demise necessitated a state rescue, shattered European confidence. Now, Europeans are discussing their banking sector. A meeting of eurozone ministers Oct. 21 is largely dedicated to the topic, as is the Oct. 23 summit of EU heads of government. Yet European governments continue to consider the banking sector largely only within the context of the ongoing sovereign debt crisis.

This is exemplified in Europeans’ handling of the Greek situation. The primary reason Greece has not defaulted on its nearly 400-billion euro sovereign debt is that the rest of the eurozone is not forcing Greece to fully implement its agreed-upon austerity measures. Withholding bailout funds as punishment would trigger an immediate default and a cascade of disastrous effects across Europe. Loudly condemning Greek inaction while still slipping Athens bailout checks keeps that aspect of Europe’s crisis in a holding pattern. In the European mind — especially the Northern European mind — a handful of small countries that made poor decisions are responsible for the European debt crisis, and while the ensuing crisis may spread to the banks as a consequence, the banks themselves would be fine if only the sovereigns could get their acts together.

This is an incorrect assumption. If anything, Europe’s banks are as damaged as the governments that regulate them.

When evaluating a problem of such magnitude, one might as well begin with the problem as the Europeans see it — namely, that their banks’ biggest problem is rooted in their sovereign debt exposure.

The state-bank contagion problem is fairly straightforward within national borders. As a rule the largest purchaser of the debt of any particular European government will be banks located in the particular country. If a government goes bankrupt or is forced to partially default on its debt, its failure will trigger the failure of most of its banks. Greece does indeed provide a useful example. Until Greece joined the European Union in 1981, state-controlled institutions dominated its banking sector. These institutions’ primary reason for being was to support government financing, regardless of whether there was a political or economic rationale justifying that financing. The Greeks, however, have no monopoly on the practice of leaning on the banking sector to support state spending. In fact, this practice is the norm across Europe.

Spain’s regional banks, the cajas, have become infamous for serving as slush funds for regional governments, regardless of the government in question’s political affiliation. Were the cajas assets held to U.S. standards of what qualifies as a good or bad loan, half the cajas would be closed immediately and another third would be placed in receivership. Italian banks hold half of Italy’s 1.9 trillion euros in outstanding state debt. And lest anyone attempt to lay all the blame on Southern Europe, French and Belgian municipalities as well as the Belgian national government regularly used the aforementioned Dexia in a somewhat similar manner.

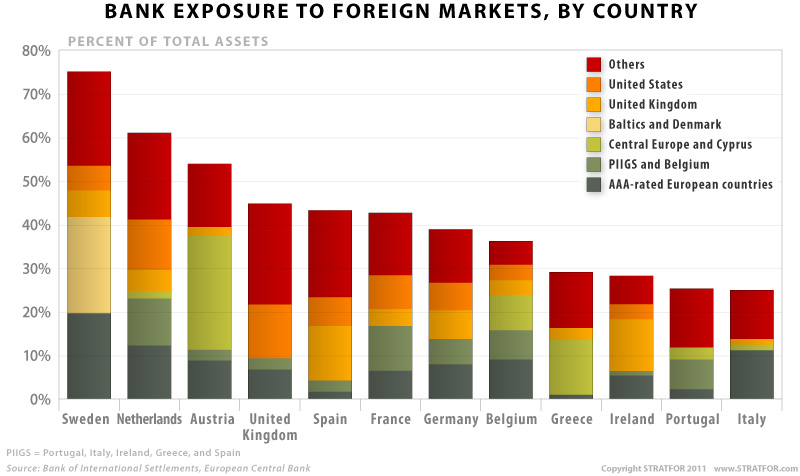

Yet much debt remains for outsiders to own, so when states crack, the damage will not be held internally. Half or more of the debt of Greece, Ireland, Portugal, Italy and Belgium is in foreign hands, but like everything else in Europe the exposure is not balanced evenly — and this time, it is Northern Europe, not Southern Europe, that is exposed. French banks are more exposed than any other national sector, holding an amount equivalent to 8.5 percent of French gross domestic product (GDP) in the debt of the most financially distressed states (Greece, Ireland, Portugal, Italy, Belgium and Spain). Belgium comes in second with an exposure of roughly 5.5 percent of GDP, although that number excludes the roughly 45 percent of GDP Belgium’s banks hold in Belgian state debt.

When Europeans speak of the need to recapitalize their banks, creating firebreaks between cross-border sovereign debt exposure dominates their thoughts — which explains why the Europeans belatedly have seized upon the IMF’s original 200 billion-euro figure. The Europeans are hoping that if they can strike a series of deals that restructure a percentage of the debt owed by the Continent’s most financially strapped states, they will be able to halt the sovereign debt crisis in its tracks.

This plan is flawed. The figure, 200 billion euros, will not cover reasonable restructurings. The 50 percent writedowns or “haircuts” for Greece under discussion as part of a revised Greek bailout — likely to be announced at the end of the upcoming Oct. 23 EU summit — would absorb more than half of that 200 billion euros. A mere 8 percent haircut on Italian debt would absorb the remainder.

Moreover, Europe’s banking problems stretch far beyond sovereign debt. Before one can understand just how deep those problems go, we must examine the role European banks play in European society.

The Centrality of European Banking

Several differences between the European and American banking sectors exist. By far the most critical difference is that European banks are much more central to the functioning of European economies than American banks are to the U.S. economy. The reason is rooted in the geography of capital.

Maritime transport is cheaper than land transport by at least an order of magnitude once the costs of constructing road and rail infrastructure is factored in. Therefore, maritime economies will always have surplus capital compared to their land transport-based equivalents. Managing such excess capital requires banks, and so nearly all of the world’s banking centers form at points on navigable rivers where capital richness is at its most extreme. For example, New York is where the Hudson meets the Atlantic Octen, Chicago is at the southernmost extremity of the Great Lakes network, Geneva is near the head of navigation of the Rhone, and Vienna is located where the Danube breaks through the Alps-Carpathian gap.

Unity differentiates the U.S. and European banking system. The American maritime network comprises the interconnected rivers of the Greater Mississippi Basin linked into the Intracoastal Waterway, which allows for easy transport from the U.S.-Mexico border on the Gulf of Mexico all the way to the Chesapeake Bay. Europe’s maritime network is neither interlinked nor evenly shared. Northern Europe is blessed with a dozen easily navigable rivers, but none of the major rivers interconnect; each river, and thus each nation, has its own financial capital. The Danube, Europe’s longest river, drains in the opposite direction but cuts through mountains twice in doing so. Some European states have multiple navigable rivers: France and Germany each have three major ones. Arid and rugged Spain and Greece, in contrast, have none.

The unity of the American transport system means that all of its banks are interlinked, and so there is a need for a single regulatory structure. The disunity of European geography generates not only competing nationalities but also competing banking systems.

Moreover, Americans are used to far-flung and impersonal capital funding their activities (such as a bank in New York funding a project in Nebraska) because of the network’s large and singular nature. Not so in Europe. There, regional competition has enshrined banks as tools of state planning. French capital is used for French projects and other sources of capital are viewed with suspicion. Consequently, Americans only use bank loans to fund 31 percent of total private credit, with bond issuances (18 percent) and stock markets (51 percent) making up the balance. In the eurozone roughly 80 percent of private credit is bank-sourced. And instead of the United States’ single central bank, single bank guarantor and fiscal authority, Europe has dozens. Banking regulation has been expressly omitted from all European treaties to this point, instead remaining a national prerogative.

As a starting point, therefore, it must be understood that European banks are more central to the functioning of the European system than American banks are to the American system. And any problems that might erupt in the world of European banks will face a far more complicated restitution effort cluttered with overlapping, conflicting authorities colored by national biases.

Demographic Limitations

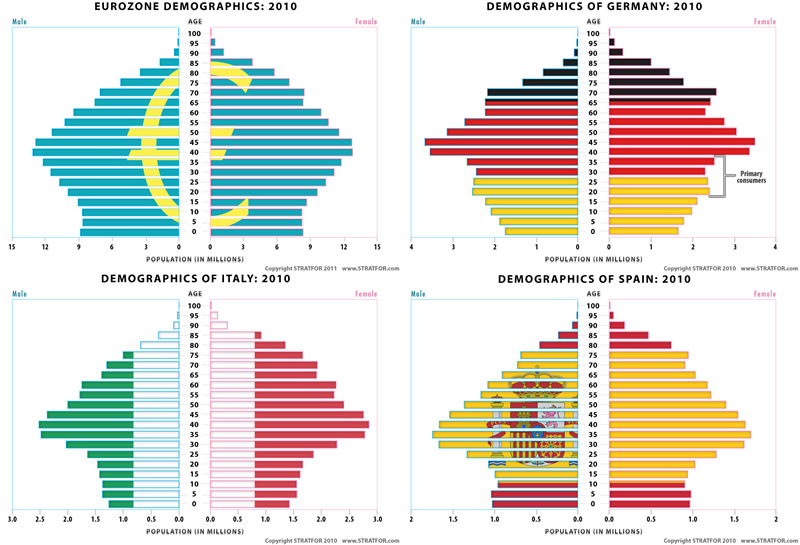

European banks also face less long-term growth. The largest piece of consumer spending in any economy is done by people in their 20s and 30s. This cohort is going to college, raising children and buying houses and cars. Yet people in their 20s and 30s are the weakest in terms of earning potential. High consumption plus low earning leads invariably to borrowing, and borrowing is banks’ mainstay. In the 1990s and 2000s much of Europe enjoyed a bulge in its population structure in precisely this young demographic — particularly in Southern European states — generating a great deal of economic activity, and from it a great deal of business for Europe’s banks.

But now, this demographic has grown up. Their earning potential has increased, while their big surge of demand is largely over, sharply curtailing their need for borrowing. In Spain and Greece, the younger end of population bulge is now 30; in Italy and France it is now 35; in Austria, Germany and the Netherlands it is 40; and in Belgium it is 45. Consumer borrowing in general and mortgage activity in particular probably have peaked. The small sizes of the replacement generations suggests there will be no recoveries within the next few decades. (Children born today will not hit their prime consumptive age for another 20 to 30 years.) With the total value of new consumer loans likely to stagnate (and more likely, decline) moving forward, if anything there are now too many European banks competing for a shrinking pool of consumer loans. Europe is thus not likely to be able to grow out of any banking problems it experiences. The one potential exception is in Central Europe, where the population bulges are on average 15 years younger than in Western Europe. The younger edge of the Polish bulge, for example, is only 25. In time, these states may be able to grow out of their problems. Either way, the most lucrative years for Western European banking are over.

Too Much Credit

Germany has extremely high capital accumulation and extremely competent economic management. One of the many results of this pairing is extremely inexpensive capital costs. When Germans — governments, corporations or individuals — borrow money, it is accepted as a near-fact that they will pay back what they owe, on time and in full. Reflecting the high supply and low risk, German borrowing rates for governments and corporations have long been in the low to mid single digits.

The further you move from Germany the less this pattern holds. Capital availability shrivels, management falters and the attitude toward contract law (or at least as defined by the Germans) becomes far less respectful. As such, Europe’s peripheral economies — most notably its smaller peripheral economies — have normally faced higher borrowing costs. Mortgage rates in Ireland stood near 20 percent less than a generation ago. Government borrowing rates in Greece have in the past topped 30 percent.

With that sort of difference, it is not difficult to see why many European states have striven for inclusion in first, the European Union, and second, the eurozone. Each step of the European integration process has brought them closer in financial terms to the ultra-low credit costs of Germany. The closer the German association, the greater the implicit belief that German financial resources would help them in a crisis (despite the fact that EU treaties explicitly rejected this).

The dawn of the eurozone era prompted lenders and investors to take this association to an extreme. Association with Germany shifted from lower lending rates to identical lending rates. The Greek government could borrow at rates that only Germany could demand in the past. Irish borrowers were able to qualify for 130 percent mortgages at 4 percent. Compounding matters, the collapse of borrowing costs and the explosion of loan activity occurred at the same time as Southern Europe’s demographic-driven consumption boom. It was the perfect storm for explosive banking growth, and it laid the groundwork for a financial collapse of unprecedented proportions.

Drastic increases in government debt are the most publicly visible outcome, but it is far from the only one. The least visible outcome is that extraordinarily cheap credit to consumers triggers an explosion in demand that local businesses cannot hope to fill. The result is unprecedented trade deficits as money borrowed from foreigners is used to purchase foreign goods. Cyprus, Greece, Portugal, Bulgaria, Romania, Lithuania, Estonia and Spain — all states whose cheap labor when compared to the Western European core should encourage them to be massive exporters — instead have run chronic trade deficits in excess of 7 percent of GDP. Most routinely broke 10 percent. Such developments do not directly harm the banks, but as credit costs return to more rational levels — and in the ongoing debt crisis borrowing costs for most of the younger EU members have tripled and more — consumption is coming to a halt. In the few European markets that demographically may be able to generate consumption-based growth in the years ahead, credit is drying up.

Foreign Currency Risk

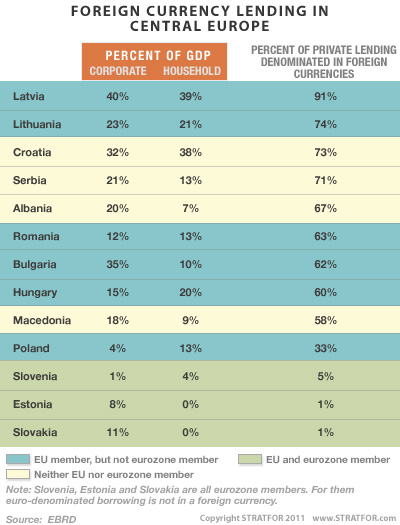

Much of this lending into weaker locations was carried out in foreign currencies. For the three states that successfully made the early sprint into the eurozone — Estonia, Slovenia and Slovakia — this was a nonfactor. For those that did not make the early leap into the eurozone it was a wonderful way to get something for nothing. Their association with the European Union resulted in the steady strengthening of their currencies. Since 2004, the Polish, Czech, Romanian and Hungarian currencies gained roughly one-third versus the euro, driving down the monthly payments on any euro-denominated loan. That inverted, however, in the 2008 financial crisis. Then, every regional currency but the Czech koruna (and Bulgarian lev, which is pegged to the euro) gave back their gains. For Central Europeans who had taken out loans when their currencies were at their highs, payments ballooned. More than 10 percent of Polish and Hungarian mortgages are now delinquent, largely because of currency movements.

New Banking ‘Empires’

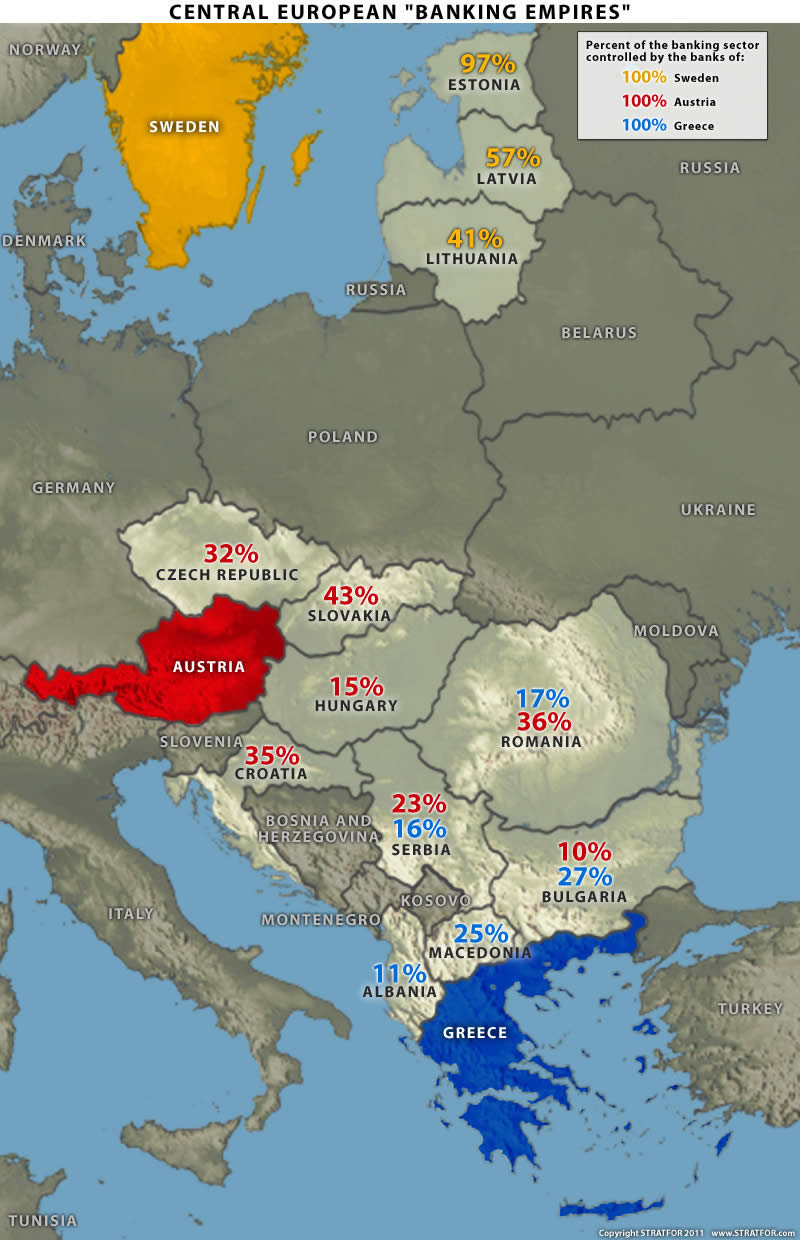

The cheap credit of the eurozone’s first decade allowed several peripheral European states a rare opportunity to expand their network of influence, even if they were not in the eurozone themselves. They could borrow money from core European banking centers like Germany, France, Switzerland and the Netherlands and pass that money on to previously credit-starved markets. In most cases, such credit was offered without the full cost-increase that these states’ poorer and smaller statures would have justified. After all, these would-be financial centers had to undercut the more established European financial centers if they were to gain meaningful market share. This pushed far more credit into Central Europe than the region otherwise would have attracted, speeding up the development process at the cost of poor underwriting and a proliferation of questionable lending practices. The most enthusiastic crafters of new banking empires have been Sweden, Austria, Spain and Greece.

- Sweden has the happiest record of any of the states that engaged in such expansionary lending. Being one of the richest countries in Europe and yet not being a member of the eurozone, Sweden did not experience a credit expansion nearly as much as other states, instead it served as a conduit for that credit — augmented by its own — to its former imperial territories. Alone among the forgers of new banking empires, Sweden’s superior financial stability has allowed it (so far) to continue financial activities in its target markets — Estonia, Latvia, Lithuania and Denmark — despite the ongoing financial crisis. But instead of lending, Swedish banks are now purchasing regional banks outright. Swedish command of the Danish banking sector, for example, has increased by 80 percent since the crisis. Through its new local subsidiaries, Swedish banks now lend more in per capita terms to Danes than they do to their own citizens, and there is no longer a domestic Estonian banking sector — it is 97 percent Swedish-owned. Such expansionary activity is likely to continue so long as Sweden can sustain it, as there is a geopolitical angle to Sweden’s effort: It is seeking to deepen its regional influence not only for economic purposes, but also to mitigate the rising role of its longtime competitor, Russia.

- Austria has tapped not only eurozone credit but also taken advantage of favorable carry trades to serve as a conduit for Swiss franc credit into Central Europe. Just as Sweden is using foreign capital to re-create its historic sphere of influence in the Baltic, Austria is doing the same in the lands of the former Austro-Hungarian Empire. Now, the majority of all mortgages in Poland, Hungary, Croatia and Romania — and a sizable minority in Austria — are denominated in foreign currencies, courtesy of Austrian banking activity. With the Swiss franc now locked in at record highs, many of these mortgages are not serviceable. The Hungarian government has felt forced to abrogate the terms of many of these loans, knowing that the Austrian banks are now so overexposed to Central Europe that they have no choice but to take the losses. As the financial crisis has continued apace, Austria has found itself with more exposure, fewer domestic resources and greater vulnerability to external forces than Sweden. So instead of being able to take advantage of regional weakness, it is finding itself losing market share both at home and in its would-be financial empire to Russia.

- Spain’s banking empire isn’t even in Europe. Spanish firms BBVA-Compass and Santander have used the cheap euro credit to massively expand credit to Latin America. And Spain’s expansion took a somewhat novel route: The combination of cheap lending at home and in Latin America encouraged more than a million Latin American Spanish speakers to relocate to Spain and gain citizenship. To smooth the naturalization process, Madrid mandated that the new Spaniards be granted top-notch credit, a factor that only added to an already hyperactive construction sector. Spanish banks’ nearly 500 billion-euro exposure to Latin America is, for now, holding; only time will tell its impact to Spain’s bottom line.

- The Greek government used its access to cheap credit to build up debt levels that are now the subject of much discussion across Europe. But much less is made of its banks, who encouraged consumers both at home and across the southern Balkans to increase their own debt levels. Being the least experienced of the four would-be financial centers, Greek banks offered the steepest credit breaks to the countries with the weakest repayment potential. Like Spain, Greece also did not make EU membership a condition for lending; vast volumes accordingly were fed into Macedonia, Serbia and even Albania

Housing Bubbles

Large volumes of suddenly cheap credit made available to eager consumers obviously generated a series of sizable housing bubbles.

Spain’s tapping of European credit markets also underwrote the largest housing boom in Europe. More construction projects have been completed in Spain in recent years than in Germany, France, Italy and the United Kingdom combined. The construction sector — both commercial and residential — has now collapsed and there are about 1 million homes now sitting vacant in a country with just 16.5 million families. Outstanding loans to various real estate interests total some 400 billion euros, all backed by collateral that has lost 20 percent of its value since the housing market peaked.

In relative terms, Ireland actually did more than Spain. At its peak, nearly 10 percent of Irish gross national product was dependent upon construction, with 70 percent of that purely from residences. Half of the mortgages extended during the Irish real estate boom were made at the peak of the market between 2006 and 2008. That sector remains in the midst of a fairly rapid collapse. Residential home prices have reduced by half since their peak in 2007 and are showing few signs of stabilizing. The Irish government hopes that with their eurozone bailout package, their banking sector will become functional again by 2020. Until then, Ireland in effect has no banking sector and has been financially sequestered from the rest of the eurozone.

Two other European states — the United Kingdom and Sweden — have both experienced massive increases in home price growth, and both suffered from price corrections due to the 2008 financial crisis. But prices in both markets have recovered smartly, with Sweden even bouncing back above its pre-crisis highs. Sweden, in fact, is still experiencing a massive housing boom, with annual mortgage credit still expanding at a 30 percent annualized rate.

Next: Looking Ahead in the European Banking Crisis

By George Friedman

This analysis was just a fraction of what our Members enjoy, Click Here to start your Free Membership Trial Today! "This report is republished with permission of STRATFOR"

© Copyright 2011 Stratfor. All rights reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis.

STRATFOR Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.