Peak Oil or Peak Energy? – Global Shale Oil Solution

Commodities / Crude Oil Dec 11, 2012 - 03:38 AM GMTBy: John_Mauldin

A consistent theme in this letter has been the connections between items that may seem to be far removed from each other but are actually linked at the very core. If you push on one end you get a reaction in what would seem to be the most unlikely spots. Today we explore the connection between the fiscal deficit and energy policy. Everyone in Washington is starting to “get religion” about wanting to fix the deficit, with serious thinkers on all sides acknowledging that there must be reform and a path to a balanced budget. Burgeoning healthcare and Social Security costs are rightly pointed to as the problem, and entitlement reform will soon be front and center.

A consistent theme in this letter has been the connections between items that may seem to be far removed from each other but are actually linked at the very core. If you push on one end you get a reaction in what would seem to be the most unlikely spots. Today we explore the connection between the fiscal deficit and energy policy. Everyone in Washington is starting to “get religion” about wanting to fix the deficit, with serious thinkers on all sides acknowledging that there must be reform and a path to a balanced budget. Burgeoning healthcare and Social Security costs are rightly pointed to as the problem, and entitlement reform will soon be front and center.

But the fiscal (government) deficit in the US cannot go away unless we also deal with the trade deficit. As we will see, it is a simple accounting issue, and one based on 400 years of accepted accounting principles. And dealing with the trade deficit in the US means working with our energy policy.

The trade imbalances among the partners in the eurozone are at the heart of the problems there as well. And while we will get back to Europe in a few weeks (remember when we seemed to be focused on Europe and Greece for months on end?), today we will explore the trade problem from a US perspective. Happily, this problem, while serious, does have a workable solution. And it might even happen in spite of government policy, though if a proactive energy policy were developed, it could ignite a true economic renaissance.

I have been wanting to explore the implications of the shale oil revolution. Old oil fields are wearing out, as peak oil advocates point out. Where can we find the huge and cheap-to-exploit oil fields to replace them? Hasn’t all the easy oil already been found? We will start in the Texas of my youth, journey to North Dakota where I was last week, and then think about the implications of that journey. There are many connections and interesting paths to explore. The letter will print a little long, as there are a lot of charts.

Looking Over My Shoulder

But first, this is the month when economists and investment analysts trot out their annual forecasts. I traditionally make mine the first week in January, after I read scores of other forecast the last three weeks of the year. It’s just something I have done for many years. I make a point of reading those I suspect I might disagree with to help me with my own thinking. It helps keep me in the middle of the road.This year you can share in that experience with me, if you like. I publish a service called Over My Shoulder, in which I highlight 5-10 items a week (out of the hundred or more that I read) that I think are worthy of your attention. My reading is quite eclectic and broad, which is reflected in my choices for posting. The subscribers to Over My Shoulder have given me very positive feedback, for which I am grateful.

In essence, I act as your personal filter for news that is important to your investments and money management, generally from sources you won’t encounter in your own regular reading. This year in OMS I will highlight what I think are some of the better and more well-reasoned annual forecasts. I think you will find it quite useful. You can subscribe by going here. I am often told I should charge more for the service, but I think it is a reasonable price. I certainly charge less than I would if I were paying someone else to round up these pieces, and you get access to all my sources, some of which are quite pricey. You can subscribe risk-free and read and think along with me about the coming year. And now, come along with me to the Bakken.

It Takes an Entrepreneur

First though, I have to take you back to Wise County, Texas, about 60 miles west of Fort Worth. A Greek goat herder named Savas Paraskivoupolis (who changed his name to Mitchell) came to Galveston in 1905. His son George Mitchell worked his way through Texas A&M and got a degree in petroleum engineering. After the war, George teamed up with his brother Johnnie and Merlyn Christie. They drilled their first well in 1952, in what became known as the Boonesville Field in Wise County, near Bridgeport where I grew up. They went on to drill hundreds of gas wells but had to shut them down because they had no way to deliver the natural gas they found in abundance. The work was done at serious financial risk, but they just kept drilling and plugging those wells. Finally a contract for a pipeline was financed by an Illinois utility, and those wells went into production.What started as Christie, Mitchell and Mitchell soon became a major employer in my little hometown and a powerful spur to the local economy. The future father-in-law of my childhood best friend was first permanent North Texas employee, back in the early 1950s, and he was eventually joined by the fathers of many of my friends.

Over the coming years Mitchell would drill over 10,000 wells, with over 1000 of them being wildcat or exploratory wells. He is a legend. His story is reminiscent of that of Walt Disney, who also lived constantly on the edge of crisis in the early days of his business. In the late ’80s and early ’90s Mitchell pioneered a new drilling method called horizontal drilling. It is still hard for me to imagine, that there is a small amount of flexibility in what seems like rigid steel pipe. Over hundreds of feet of drilling, they can turn a pipe inch by inch until it describes a 90° arc.

Everyone knew there was more gas deeper in the ground, but it was trapped in very tight shale formations. Mitchell and his engineers figured out how to put water under pressure back into the earth to create very minute fractures that allowed the gas and oil to be freed. This is the process known as hydraulic fracturing, or fracking. In the ’90s and especially the last decade, there has once again been an oil and gas boom in Wise county, in what is called the Barnett Shale. Except, the Barnett Shale is a far more massive formation than the original Boonesville field. Once again Texas was at the center of US energy production. The new technology opened up vast new reserves that were impossible to get to just a few years ago.

And then it turned out there were potentially even larger shale oil fields scattered throughout the United States – and, as we are learning, seemingly everywhere in the world. The first modern oil wells were drilled in Poland in 1854 at around 100 feet in depth, and now exploratory wells show that 11,000 to 13,000 feet below the surface there is considerably more oil and gas in Poland and the surrounding region.

In contrast to today’s deep wells, the legendary Drake Well was drilled in Titusville, Pennsylvania, in 1859 at a depth of 69 feet. And there is evidence of ancient oil drilling using bamboo pipes in China. Marco Polo remarked on bubbling springs of oil in what is now Azerbaijan.

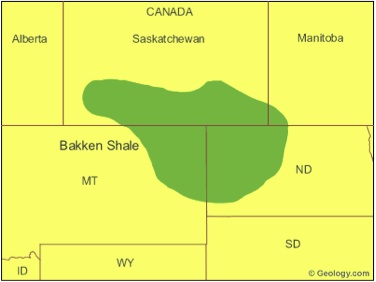

And that brings us to the Bakken shale oil and gas fields. I was invited to speak to the customers of BNC Bank in North Dakota by its president and CEO, Greg Cleveland, last week. He graciously offered to take me on a helicopter tour of the Bakken Field if I would come a day early, which I of course agreed to do. As a special bonus, he arranged for Loren Kopseng to be our tour guide. Loren didn’t drill the first well in the Bakken, but he was there by the time the third well went in, and he now owns a piece of about 20% of all the wells drilled in the region. (There are over 7,000 wells in the region and counting.)

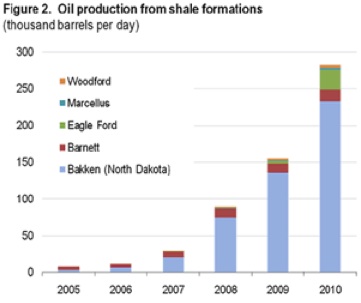

Today the Bakken overshadows the Barnett. Notice in the graph below how rapid the growth has been. More recently, permits were granted for 904 wells in August, September, and October 2012, with October being the record with 370 wells.

We flew the 50-odd miles from Bismarck to the edge of the Bakken, over the famous Badlands (which I found quietly beautiful) to what Loren called the line of death. On one side of the line, if you drilled you would get a dry hole. On the other side there is an amazing reported 99% success rate. The field stretches from western North Dakota and eastern Montana up into Saskatchewan, Canada.

The Line of Death

Easy money, right? Just punch a hole in the ground and count your money. Today, perhaps, but not in the beginning. As we were flying, Loren asked me what I knew about oil drilling. I had to admit I didn’t know much, except that my best friend Randy Scroggins from elementary school wouldn’t let me invest in his oil company in 1981.Loren laughed and said Randy was a very good friend indeed – and added that “1981 was the first time I went bankrupt.” While Loren grew up in Bismarck, he would have been at home in Texas. He is the quintessential wildcatter, straight out of central casting. There is a certain infectious enthusiasm that seems to emanate from that special breed of entrepreneur called an oil man. Not only do you have to put up with the potential for drilling a dry hole, whereupon you lose all your money, you have to contend with the ups and downs in oil prices. While the major oil companies have become more conservative players, the real cutting edge is among smaller independents. And Loren is at the knife point of the cutting edge.

Flying into the heart of the field reminded me of my roots in Bridgeport. Drilling for oil is not pretty. It is actually fairly messy, although I must say there is seemingly much greater care taken to keep things neater than what I remember as a kid. Flying over completed wells, when it was just the pump and storage containers, showed a relatively small footprint, with the land being farmed right to the edge of the pad.

In my experience, oil wells were drilled pretty densely across the land, as you could only drill straight down. You basically got only the oil that was right underneath your well. In fracking shale oil, there is less need to put wells so close together. There is typically only one drilling pad for one section of land, that is, 640 acres or one square mile. Current technology is improving even on that, as a well can go down two miles and then turn horizontally another two miles.

I took the picture below my with my iPad as we were flying into this well for a tour. That drilling pad will be cleaned up and once again become part of the farmland that surrounds it today. That is a pretty massive rig, but it can be torn down, moved, and set back up in seven days.

A quick tutorial on shale oil: Global shale oil reserves are currently estimated at over three trillion barrels recoverable under current technology. The US has well over two trillion of those barrels. (Average estimates from numerous sources.)

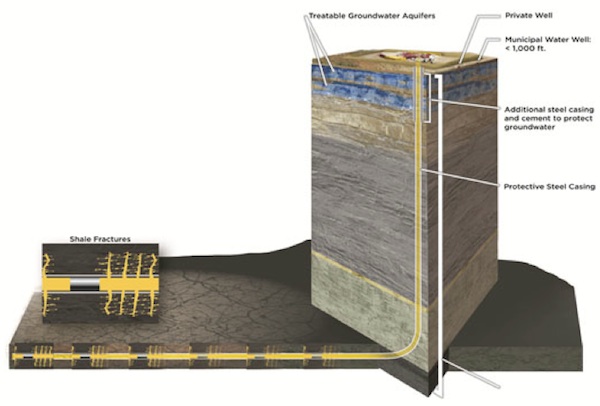

The illustration below shows the typical construction of a shale oil or gas well. Note that the drill holes are “cemented” in around the pipes so that nothing can leak into the surrounding earth. Shale oil and gas lie very deep under very nonporous layers of rock. There are very serious environmental rules about drilling and fracking (as there should be). A large portion of the drilling rig is containment for the water and other fluids that come from the drilling. The waste fluids are not dumped onto the local ground.

No serious person would allow fracking near the water table. That does not mean there is not oil and gas in the water table already. Stockton, California lighted its county courthouse in 1854 with natural gas from a local water well. California has thousands of naturally occurring seeps. In the Gulf of Mexico, there are more than 600 natural oil seeps that leak between five hundred thousand and one million barrels of oil per year. When a petroleum seep develops underwater it may form a peculiar type of volcano known as an asphalt volcano. The ecological system has evolved certain bacteria that thrive on the oil seeps. One of the interesting things about the British Petroleum oil-spill disaster in the Gulf of Mexico was the disappearance of the oil over a few years. While it was a true disaster, it is theorized that the bacteria multiplied to deal with the crisis. But it took a long time. There is no excuse for what BP did.

As far as I can research from true experts, properly done, horizontal drilling and fracking pose no danger to the environment. (That is different from saying that burning gas in our cars has no impact. Different topic. I’m all for my electric car powered by nuclear energy.)

Notice in the illustration above the small gray areas in the horizontal pipe. Loren took me to a pile of what he called “jewelry.” These are about four-foot-long marvels of technology encased in beautiful stainless steel, looking like shiny gems along the dark string of iron pipe. The first wells drilled in the Bakken had just one “jewel.” While there is some debate about how many jewels to use to maximize fracking effectiveness in a two-mile pipe, I think I remember Loren saying that they are using up to 37. (It might have been 23, but oddly, I do remember it was definitely a prime number.)

Loren simply went into raptures describing the technology in each of those jewels. Since it was 9° out, with the wind chill taking it down to about -15° and I was not appropriately dressed, I might have missed a point or two.

The US Energy Information Administration (EIA) reports that over 750 trillion cubic feet of technically recoverable shale gas and 24 billion barrels of technically recoverable shale oil have been discovered in shale plays. Except that they are reportedly having to update their update. Just five days ago they announced new projections that suggest US energy imports (as a share of production) will fall in half in the next 30 years. (This does not include any new sources of non-carbon-based energy – new technology can make estimates turn out quite wrong.)

Harold Hamm and Continental Resources drilled the first horizontal well to use fracking in the Bakken in 2004. He knows something about the region. He is now telling us that there may be four more layers (which are called benches) of shale oil and gas below the Upper Bakken formation, including the promising Three Forks stratum. Just a week ago (onDecember 3), Continental announced they had completed a well in the “third bench.” The Three Forks could be a bigger story than the Upper Bakken formation, as it is much thicker. Hamm is projecting almost a trillion barrels of reserves in the area.

What Loren thinks will happen is that the new drilling rigs that can move themselves will soon drill as many as 16 holes from one pad, into all the various levels and in different directions. Punch a hole in the ground, complete the well, move the rig over a bit and start the process again. That really helps keep down the cost of drilling, as does each bit of new technology.

Get a Job

North Dakota is the third most productive energy state, on its way to being number two, behind Texas. And that is creating jobs. Lots of jobs. Unemployment in the Bakken region is 1%. $10-15 an hour for working in a fast food restaurant, if you can even find someone to work for so little.Let me give you a rundown on what I found. When we went into the “office” of the rig there was a young man who looked to be in his early 30s. He was a “tool-pusher,” which means he ran the rig. Clearly very smart and trustworthy, but he didn’t have a college degree, just lots of oil-field experience. He works 28 days, 12 hours a day straight and then takes two weeks off to go see his wife and kids. When working he lives in a small room at the rig. He makes $350,000 a year. The kid is one of those millionaires and billionaires that Obama wants to tax.

A starting salary on the rig is $120,000 a year, with no experience. But you work your tail off for very long hours. The consultant who oversaw the rig operation for the investors made around $250,000. (By the way, he could tell me to the dollar what his costs were for the well during the hour we were there. There were very sophisticated cost controls.)

An oil-truck driver makes $150-175,000 a year. All that oil has to be taken by truck to a railroad terminal and loaded onto railcars, to form 100-car trains that take the oil to refineries around the country. Loren took us to his new train terminal, where the trucks were lined up to empty their tanks and go back to another well for a load. All up and down the line, there are jobs that are begging to be filled.

But working in the oil field is hard work and a difficult life. That starter oil-rig job? It looked quite dangerous to me. Campgrounds packed with small trailers are everywhere. There are “man camps,” which are glorified dormitories that can cost as much as $3,000 a month for room and board. Construction? If you can swing a hammer in the cold, you can have a job. Most people seemed to work for 14 or 28 days (12 hours) and then take a week or two off.

Within a few hours of being in Bismarck, my son Chad was offered a job at about 50% more than he could make here in Dallas. (The local bank president took him and another man on a tour of Bismarck while I was in the air, so Chad did have some job-hunting help.)

I went to a Christmas party that night for the customers of the bank – as nice a group of people as you could want to meet, many of them local farmers who drove in for the conference. If you own a farm with mineral rights, your life has changed in recent years.

As a side note, Loren pointedly told me that Greg Cleveland (founder and chairman of BNC Bank) had loaned him $1 million to get his current business started back in 1985 when no one else would. The level of trust between these two was obvious. That night, bank customers came up and literally kissed Greg on the cheeks, while telling me how he had loaned them the money to start their businesses “back in the day.” Not just in the oil business, either. That type of banking relationship is hard to find these days. Lloyd Blankfein (Goldman Sachs CEO and chairman), eat your heart out. This is small-town banking as it’s supposed to be (we had that once in Texas).

As I noted a few weeks ago, shale gas will add about 0.5% to the growth of US GDP next year, in a year when we will be lucky to get 2%. This is a huge driver of jobs and growth. And it is not just in North Dakota; there are shale gas plays all over the US and Canada. Continental Resources announced a major new shale gas field in Oklahoma in October, comparing its geology to that of the Bakken.

The US will be exporting natural gas within 3-4 years from McAllen, Texas, and other LNG ports are in various stages of permitting. Natural gas in Japan is over $15, compared to $3.78 this morning in the US. Europe is in double digits ($11.83). There is an arbitrage available here. Even an economist can do the math.

But our real advantage may not come in exporting raw gas but rather in the chemical products you need gas to make. Not just fertilizers but feedstocks for plastics and other organic chemicals.

The Financial Times wrote last Saturday, "Europeans are already complaining that cheap US gas is encouraging a flight of energy intensive businesses [to the US]. How can, say Europe's chemical producers – buying expensive Russian gas – compete with US rivals guaranteed access to cut-price feedstock?” (Hat tip Vincent Farrell.)

One way for them to compete is, perhaps, to develop their own (seemingly considerable) shale oil and gas fields. But there seems to be a great deal of resistance to that. And that reluctance will help the US close its trade deficit.

Not Everyone Can Run a Surplus

The chart below shows that we are spending more for energy even as we use less of it, and that drives up our trade deficit. Let’s see why this matters. As long-time readers know, I have often written about how you cannot balance private and government deficits without a positive trade balance. Let me quickly review.

It is the desire of every country to somehow grow its way out of the current mess. And indeed that is the time-honored way for a country to heal itself. But let's look at an equation that shows why that might not be possible this time. We have here another case of people wanting to believe six impossible things before breakfast.

Let's divide a country's economy into three sectors: private, government, and exports. If you play with the variables a little bit, you find that you get the following equation. Keep in mind that this is an accounting identity, not a theory. If it is wrong, then five centuries of double-entry bookkeeping must also be wrong.

Domestic Private Sector Financial Balance + Governmental Fiscal Balance - the Current Account Balance (or Trade Deficit/Surplus) = 0

By Domestic Private Sector Financial Balance we mean the net balance of businesses and consumers. Are they borrowing money, or paying down debt? Government Fiscal Balance is the same: is the government borrowing, or paying down debt? And the Current Account Balance is the trade deficit or surplus.

The implications are simple: the three items have to add up to zero. That means you cannot have surpluses in both the private and government sectors and run a trade deficit; you have to have a trade surplus.

Let's make this simple. Let's say that the private sector runs a $100 surplus (they pay down debt), as does the government. Now, we subtract the trade balance. To make the equation come to zero there must be a $200 trade surplus:

$100 (private debt reduction) + $100 (government debt reduction) - $200 (trade surplus) = 0.

But what if the country wanted to run a $100 trade deficit? Then either private or public debt would have to increase by $100. The numbers have to add up to zero. One way for that to happen would be:

$50 (private debt reduction) + (-$150) (government deficit) - (-$100) (trade deficit) = 0. (Note that we are adding a negative number and then subtracting a negative number.)

Bottom line: you can run a trade deficit, reduce government debt, or reduce private debt, but not all three at the same time. Choose two. Choose carefully.

Peak Oil or Peak Energy? – A Happy Solution

The US is lucky; there is plenty of oil and gas below our borders, with much of it in private hands. There are estimates the US could be energy independent within 7-10 years. But it will not be easy. Skeptic Arthur Berman recently presented Oil-Prone Shale Plays: The Illusion of Energy Independence. He estimates that it will take 1,488 new wells a year in the Bakken just to replace the oil currently produced there, as wells deplete over time. He argues (quite well) that the US will not become energy independent. You can read his report at http://www.sipeshouston.org/Presentations.sh.sem.10.2012/8%20Oil%20Shale.pdfHis analysis suggests that oil prices will have to remain high or go even higher for shale oil to be profitable. I think he is right on that. I have always maintained that we are not likely to run out of oil for a very long time; we will just run out of cheap oil. Thankfully, there are alternatives being developed over time. The cost of producing solar energy has dropped about 50% per decade for a long time. In another few decades solar will be quite competitive with carbon-based energy. Nuclear remains my favourite shorter-term source, but it confronts considerable political opposition in many countries.

But in the meantime, we should open up public lands for commercial drilling. And we should do it for a price. Texas finances a great deal of its higher education from oil and gas royalties for wells on state land. US government land should be used to produce revenue as well. New technologies allow for environmentally sensitive use of land. Not only will increased drilling produce needed revenue from royalties and taxes, it will create jobs and allow the possibility of eliminating the trade deficit. What a happy solution! And compared to healthcare, this should be easy!

And why do I think all this can happen? Because of the cast of characters who will keep raising money and drilling for oil and gas. Guys like Loren Kopseng and Harold Hamm, who are just a force of nature and will get it done. These are the true entrepreneurs, who are the main source of our new jobs. If we can keep them from being saddled with too-high taxes and too many rules, they will build that future for us.

There are scores if not hundreds of these larger-than-life characters, with a few good bankers like Greg Cleveland to back them. Let’s turn them loose!

New York, Cleveland, and Europe

I will leave Tuesday for a trip to NYC to meet with my partners in Mauldin Economics to do our own annual planning and forecast work. The recent webinar was well-received and -reviewed (start here). The next week I jump to LA/San Diego for a planning session with Jon Sundt and my partners at Altegris. I can honestly say I have never been as excited about the prospects for a coming year. There are so many great new things we will be doing. But as with Christmas presents, I can’t tell you – it would spoil the surprise.I will be on Tom Keene at 6 AM Eastern on Wednesday, so no late night for me. Thursday I go to Cleveland to stay with Dr. Mike Roizen for a night and then have some doctors poke and prod me on Friday, before heading back home.

As a side note, I have run across an odd statistic. Long-time readers know that I have recommended a face cream with stem cells in it. It really does rejuvenate the skin. It turns out that over 50% of the customers are men. That was a surprise. I hear great reviews and receive thanks from all over from people who use it. It makes a great Christmas present. Go to https://www.lifelineskincare.com/content/ahead-curve-december-2012 to get yours at a very special price for the season. You will be glad you did!

Today we had a birthday party for my granddaughter Lively, who turned three this week. There were 16 people at the brunch table at Del Frisco’s Grille (my new favourite Sunday brunch place – awesome food!). All seven kids once again, along with significant others, grandkids, et al.

It is very interesting to watch your kids grow up, have their own successes, and deal with their problems. I remember struggling as a young man and watching my dad struggle as well. Those days back in Bridgeport? He owned a very nice gravel trucking business but went bankrupt in the late ’50s and had to start over. It was tough on him at 50 years of age to start again, and we struggled to make ends meet. I had to go to work very early. It was good for me, as I look back, but I have tried to help my kids not to have to deal with some of the same concerns. And I will admit I would not have minded a little help with college.

I think Chad is going to move to Bismarck after the holidays. Abbi is getting married in the spring and will stay in Tulsa. Amanda will bring another granddaughter into my life in the spring, too. She just took it upon herself to decorate my house for Christmas, and it looks the best it ever has. And the tree, for whatever reason, is especially fragrant this year. Changes are everywhere and yet some things stay the same. And that’s the way I like it.

I was reminded of that last week, when I spent the day with Newt Gingrich in DC. Of course we talked about the current political scene and the fiscal problems. He always seems to have a particular story from history to illustrate his views. But what we talked about the most was not the past or the present but the future. And not the political future but our shared enthusiasm for the accelerating pace of technological change. There is just so much to be optimistic about, even as we worry over the current economic issues.

I am working with Bill Dunkelberg on our book on the future of employment, and I will then turn to writing my book on where the world will be in 20 years. This one has been in the planning stages for far too long. No one in 20 years will want to go back to the good old days of 2012. I know people sometimes think (wrongly) that I am of a bearish disposition, but that is just not true. I am just bearish on governments.

Europe will be a whirlwind. Norway, Copenhagen, Sweden for the Skagen Funds, and then on to Dublin for the weekend. And then to London for an evening meeting, followed by meetings in Greece. I have my travel plans laid out except for Europe, January 16-20. If you have a suggestion or a media contact, let me know. And on the 20th I go to Geneva before heading back to Dallas on the 22nd. Quite the trip.

Have a great week, and hopefully you’ll be home for the season. All the best.

Your strangely wishing he had more time in Bismarck,

John Mauldin

subscribers@MauldinEconomics.com

Outside the Box is a free weekly economic e-letter by best-selling author and renowned financial expert, John Mauldin. You can learn more and get your free subscription by visiting www.JohnMauldin.com.

Please write to johnmauldin@2000wave.com to inform us of any reproductions, including when and where copy will be reproduced. You must keep the letter intact, from introduction to disclaimers. If you would like to quote brief portions only, please reference www.JohnMauldin.com.

John Mauldin, Best-Selling author and recognized financial expert, is also editor of the free Thoughts From the Frontline that goes to over 1 million readers each week. For more information on John or his FREE weekly economic letter go to: http://www.frontlinethoughts.com/

To subscribe to John Mauldin's E-Letter please click here:http://www.frontlinethoughts.com/subscribe.asp

Copyright 2012 John Mauldin. All Rights Reserved

Note: John Mauldin is the President of Millennium Wave Advisors, LLC (MWA), which is an investment advisory firm registered with multiple states. John Mauldin is a registered representative of Millennium Wave Securities, LLC, (MWS), an FINRA registered broker-dealer. MWS is also a Commodity Pool Operator (CPO) and a Commodity Trading Advisor (CTA) registered with the CFTC, as well as an Introducing Broker (IB). Millennium Wave Investments is a dba of MWA LLC and MWS LLC. Millennium Wave Investments cooperates in the consulting on and marketing of private investment offerings with other independent firms such as Altegris Investments; Absolute Return Partners, LLP; Plexus Asset Management; Fynn Capital; and Nicola Wealth Management. Funds recommended by Mauldin may pay a portion of their fees to these independent firms, who will share 1/3 of those fees with MWS and thus with Mauldin. Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest with any CTA, fund, or program mentioned here or elsewhere. Before seeking any advisor's services or making an investment in a fund, investors must read and examine thoroughly the respective disclosure document or offering memorandum. Since these firms and Mauldin receive fees from the funds they recommend/market, they only recommend/market products with which they have been able to negotiate fee arrangements.

Opinions expressed in these reports may change without prior notice. John Mauldin and/or the staffs at Millennium Wave Advisors, LLC and InvestorsInsight Publishing, Inc. ("InvestorsInsight") may or may not have investments in any funds cited above.

Disclaimer PAST RESULTS ARE NOT INDICATIVE OF FUTURE RESULTS. THERE IS RISK OF LOSS AS WELL AS THE OPPORTUNITY FOR GAIN WHEN INVESTING IN MANAGED FUNDS. WHEN CONSIDERING ALTERNATIVE INVESTMENTS, INCLUDING HEDGE FUNDS, YOU SHOULD CONSIDER VARIOUS RISKS INCLUDING THE FACT THAT SOME PRODUCTS: OFTEN ENGAGE IN LEVERAGING AND OTHER SPECULATIVE INVESTMENT PRACTICES THAT MAY INCREASE THE RISK OF INVESTMENT LOSS, CAN BE ILLIQUID, ARE NOT REQUIRED TO PROVIDE PERIODIC PRICING OR VALUATION INFORMATION TO INVESTORS, MAY INVOLVE COMPLEX TAX STRUCTURES AND DELAYS IN DISTRIBUTING IMPORTANT TAX INFORMATION, ARE NOT SUBJECT TO THE SAME REGULATORY REQUIREMENTS AS MUTUAL FUNDS, OFTEN CHARGE HIGH FEES, AND IN MANY CASES THE UNDERLYING INVESTMENTS ARE NOT TRANSPARENT AND ARE KNOWN ONLY TO THE INVESTMENT MANAGER.

John Mauldin Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.