Peak Prosperity - The Fed Can Only Fail. And We'll All Lose

Economics / US Debt Oct 26, 2013 - 10:43 AM GMTBy: Dr_Martenson

The basic predicament we are in is that the current crop of leaders in the halls of monetary and political power does not appear to understand the dimensions of our situation.

The basic predicament we are in is that the current crop of leaders in the halls of monetary and political power does not appear to understand the dimensions of our situation.

The mind-boggling part about all this is that it's not really all that hard to grasp.

Our collective predicament is simply this: Nothing can grow forever.

Sooner or later, everything must cease growing, or it will exhaust its environs and thereby destroy itself. The Fed is busy doing everything in its considerable power to get credit (that is, debt) growing again so that we can get back to what it considers to be "normal."

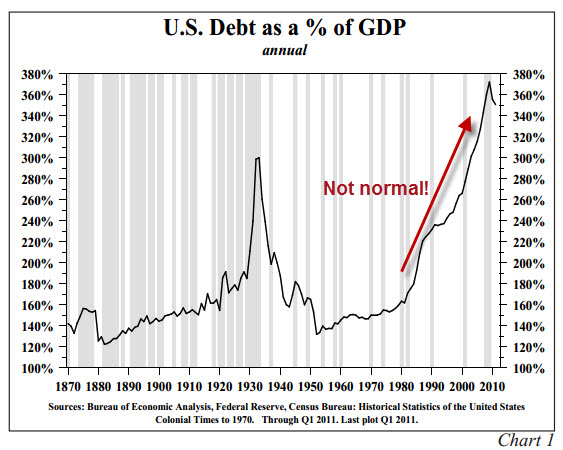

But the problem is – or the predicament, I should more accurately say – is that the recent past was not normal. You've probably all seen this next chart. It shows total debt in the U.S. as a percent of GDP:

(Source)

Somewhere right around 1980, things really changed, and debt began climbing far faster than GDP. And that, right there, is the long and the short of why any attempt to continue the behavior that got us to this point is certain to fail.

It is simply not possible to grow your debts faster than your income forever. However, that's been the practice since 1980, and every current politician and Federal Reserve official developed their opinions about 'how the world works' during the 33-year period between 1980 and 2013.

Put bluntly, they want to get us back on that same track, and as soon as possible. The reason? Because every major power center, be that in D.C. or on Wall Street, tuned their thinking, systems, and sense of entitlement during that period. And, frankly, a huge number of financial firms and political careers will melt away if/when that credit expansion finally stops.

And stop it will; that's just a mathematical certainty. It's now extremely doubtful that the Fed or D.C. will willingly cease the current Herculean efforts towards reviving this flawed practice of borrowing too much, too fast. So we have to expect that it will be some form of financial accident that finally breaks the stranglehold of failed thinking that infects current leadership.

The Math

As a thought experiment, let's explore the math a little bit to see where it leads us. After all, I did just say that a poor end to all of this is a "mathematical certainty," so let's test that theory a bit. I think you'll find this both interesting and useful.

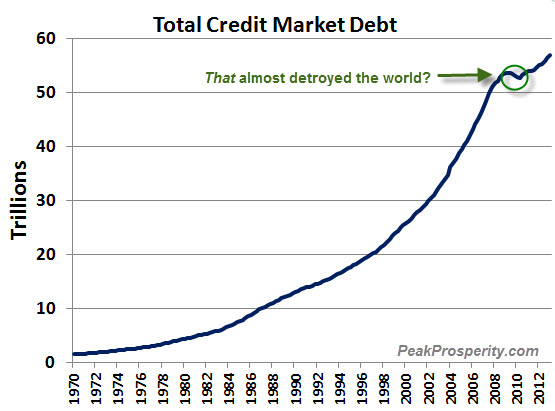

To begin, Total Credit Market Debt (TCMD) is a measure of all the various forms of debt in the U.S. That includes corporate, state, federal, and household borrowing. So student loans are in there, as are auto loans, mortgages, and municipal and federal debt. It's pretty much everything debt-related.

What it does not include, though, are any unfunded obligations, entitlements, or other types of liabilities. So the Social Security shortfalls are not in there, nor are the underfunded pensions at the state or corporate levels. TCMD is just debt, plain and simple.

As you can see in this next chart, since 1970, TCMD has been growing exponentially and almost perfectly, too. (The R2 is over 0.99, for you science types):

I've pointed out the tiny little wiggle that happened in 2008-2009, which apparently nearly brought down the entire global financial system. That little deviation was practically too much all on its own.

Now debts are climbing again at a quite nice pace. That's mainly due to the Fed monetizing U.S. federal debt just to keep things patched together.

As an aside, based on this chart, we'd expect the Fed to not end their QE efforts until and unless households and corporations once more engage in robust borrowing. The system apparently 'needs' this chart to keep growing exponentially, or it risks collapse.

Okay, one could ask: Why can't credit just keep growing?

Here's where things get a little wonky. But if you'll bear with me, you'll see why I'm nearly 100% certain that the future will not resemble the past.

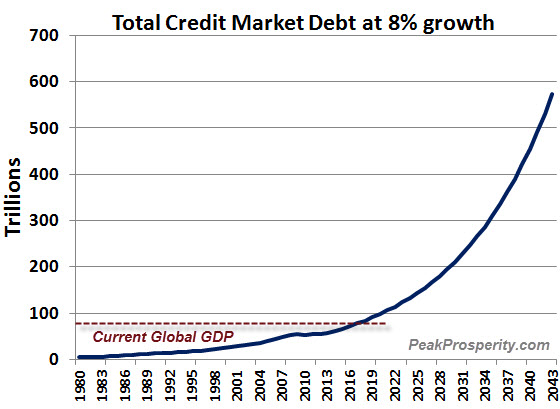

Let's start in 1980, when credit growth really took off. This period also happens to be the happy time that the Fed is trying to (desperately) recreate.

Between 1980 and 2013, total credit grew by an astonishing 8% per year, compounded. I say 'astonishing' because anything growing by 8% per year will fully double every 9 years.

So let's run the math experiment as ask what will happen if the Fed is successful and total credit grows for the next 30 years at exactly the same rate it did over the prior 30. That's all. Nothing fancy, simply the same rate of growth that everybody got accustomed to while they were figuring out 'how the world works.'

What happens to the current $57 trillion in TCMD as it advances by 8% per year for 30 years? It mushrooms into a silly number: $573 trillion. That is, an 8% growth paradigm gives us a tenfold increase in total credit in just thirty years:

For perspective, the GDP of the entire globe was just $85 trillion in 2012. Even if we advance global GDP by some hefty number, like 4% per year for the next 30 years, under an 8% growth regime, U.S. credit would be twice as large as global GDP in 2043 (!)

If that comparison didn't do it for you, then just ask yourself: Why, exactly, would U.S. corporations, households, and government borrow more than $500 trillion over the next 30 years? The total mortgage market is currently $10 trillion, so might the plan include developing an additional 50 more U.S. residential real estate markets?

More seriously, can you think of anything that could support borrowing that much money? I can't.

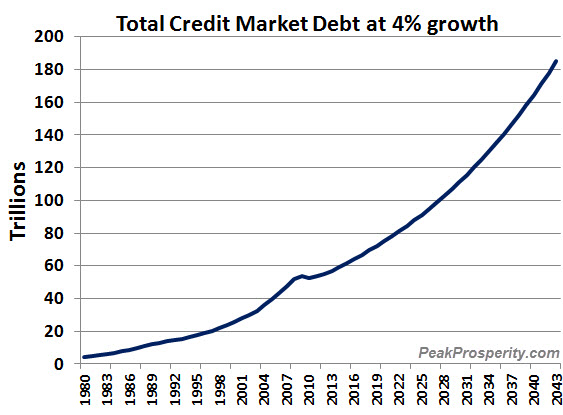

So perhaps the situation moderates a bit, and instead of growing at 8%, credit market debt grows at just half that rate. So what happens if credit just grows by 4% per year?

That gets us to $185 trillion, or another $128 trillion higher than today – a more than 3x increase:

Again, What might we borrow (only) $128 trillion for, over the next 30 years?

When I run these numbers, I am entirely confident that the rate of growth in debt between 1980 and 2013 will not be recreated between 2013 and 2043. With just one caveat: I've been assuming that dollars remain valuable. If dollars were to lose 90% or more of their value (say, perhaps due to our central bank creating too many of them?), then it's entirely possible to achieve any sorts of fantastical numbers one wishes to see.

Think it could never happen?

Conclusion (to Part I)

This is the critical takeaway from all of the math above: For the Fed to achieve anything even close to the historical rate of credit growth, the dollar will have to lose a lot of value. I truly believe this is the Fed's grand plan, if we may call it that, and it has nothing to do with what's best for the people of this land. Instead, it's entirely about keeping the financial system primed with sufficient new credit to prevent it from imploding.

That is, the Fed is beholden to a broken system; not anything noble.

In Part II: The Near Future May See One of the Biggest Wealth Transfers in Human History, we dive fully into the logic why GDP growth is very unlikely to support the rate of credit expansion that the Federal Reserve wants (or, more accurately, needs). And what will happen if it indeed doesn't? A lot of painful, awful things – but central among them is a currency crisis.

Amidst the ensuing unpleasantness will be an awakening within today's hyper-financialized markets to the huge imbalance now existing between paper claims and ownership of real things. A massive wealth transfer from those with 'paper wealth' (stocks, bonds, dollars) to those owning tangible assets (the productive value of which can't easily be inflated away) will occur – and quickly, too.

Suggesting the key objective for today's investor is answering: How do I make sure I'm on the right side of that wealth transfer?

Click here to access Part II of this report (free executive summary; enrollment required for full access).

By Dr Martenson

© 2013 Copyright Dr Martenson - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.