Themes, Dreams, and Schemes - Global Economy at Stall Speed, Monetary Velocity and Interest Rates

Economics / Global Economy Jan 16, 2016 - 04:41 PM GMTBy: Andy_Sutton

First I must offer an apology of sorts for being in absentia for an extended period of time. I would imagine that those of you who struggle to keep up with the demands of work, family, and everyday stresses understand this, but I apologize anyway. There are links on the blog to the Liberty Talk Radio appearances I’ve made over the past few months just to prove that I’m still vertical. Graham joins me once again and as always has some interesting takeaways.

First I must offer an apology of sorts for being in absentia for an extended period of time. I would imagine that those of you who struggle to keep up with the demands of work, family, and everyday stresses understand this, but I apologize anyway. There are links on the blog to the Liberty Talk Radio appearances I’ve made over the past few months just to prove that I’m still vertical. Graham joins me once again and as always has some interesting takeaways.

All the preliminaries aside, 2016 starts with yet another spat of turmoil in the markets. This has been dwelled upon to the point of making one ill so this will not be yet another analysis of The Dow Jones averages, Grand Supercycle waves, Kondratieff winters, and such. Rather we are going to spend a bit of time looking at themes. Particularly the themes we’ve been discussing and how what is going on now fits into those themes.

Secondly, we’re going to be looking at the dreaming that is being done by politicians, candidates for political office and those less informed among us. Minus hallucinogenic drugs, it is amazing to watch how people twist reality into something that fits their mindset, agenda, or whatever. We have literally gotten to the point in time where there is no actual truth anymore – if you choose to listen to the masses. The sky is still blue, and so forth, but almost NOTHING is accepted at face value as fact. This is important because it leaves EVERYTHING open to interpretation. Ours will certainly be different than someone such as Janet Yellen – a useful idiot for the establishment, which profits insanely from all this nonsense going on – regardless of the direction.

Lastly, all of the above are the result of schemes. We’ve discussed the big ones such as the bail-in. We’ve laid it bare from concept through implementation. The bail-in is by far not even the biggest scheme. Superceding the bail-in is the notion that the money being eyed up by the establishment for confiscation actually has value to begin with. This is a dangerous time, especially with fuel prices falling. People perceive that as actual monetary deflation when it is nothing of the sort. Again, we are back to the arena of facts being a debating society. Nothing is concrete. Does this seem to be an accident? We think not. In fact we know it isn’t.

Theme #1 – Global Economy at Stall Speed

Central bankers love to use fancy terms like ‘escape velocity’. That a bunch of con artists ripped off some rocket scientists (Really!) is quite hilarious. The average person listens to these fancy schmancy speeches and says ‘Wow, that guy sounds really smart; he must know what he’s talking about”. He sure does, but is he really telling you the TRUTH? We’ve contended time and time again that central bankers and those in the establishment are not stupid people. Far from it. They are geniuses in fact. If they’d put their considerable brainpans to work solving problems instead of creating them we’d be much better off, but that is a discussion for another day.

Back in 2009 there was a segment on what was then Contrary Investor’s Café along with a concomitant ‘Two Cents’ piece entitled ‘Throttling the Recovery’. The point of focus was peak oil, fossil fuels, and the fact that due to squandering and greed there just wasn’t enough of the stuff to go around. And it isn’t just oil. That whole debate has kind of disappeared over the past few years as suddenly the globe finds itself awash in oil. Another glut in fact. But why? Is this a supply or a demand driven phenomena? Granted we’ve been punching holes in the Earth with reckless abandon to the point where the USGS actually went on record associating tremors in Oklahoma with drilling and hydraulic fracturing. The Williston Basin has been teeming with activity for nearly a decade now. It seems that everyone imaginable was trying to stick a straw through the Earth’s surface and rush whatever oil they could find to market.

But what market? The global economy has been dragging, weighed down by a multi-continent slowdown, runaway debt, geopolitical strife, and a multitude of mini-crises. These are facts. Financial markets have been in near-panic sell-off mode over the ‘news’ that China’s manufacturing sector is slowing down. Ya think? Thanks Captain Obvious. Anyone who has been paying attention knows that those who buy from China aren’t buying as much. What did the geniuses on CNBC think would happen? If we had honest reporting and honest discovery of information then the Chinese slowdown wouldn’t have been a shock to anyone at all.

And let’s get something else straight while we are at it. Those ‘investors’ we always hear about on the news? They are not 20-somethings digging Frito’s corn chips out of the sofa cushions to nourish themselves while they trade stocks on the Internet. The vast, vast majority of buying and selling of financial instruments is done by people who know all of what we’ve mentioned thus far; and even more. Most importantly, many of them know the ‘when’ and the ‘who’. They are rarely surprised.

Back to our point, however. The global economy is slow, remains slow, and with central banks potentially in a tightening trend, things will stay slow if not stall entirely. The central bankers know this. They’re not idiots, despite all the caricatures of them as such in newspapers, etc. Back in 2009, Andy made the point that it was at least possible that peak oil was causing policymakers to seek to throttle the growth of the global economy. We’d like to add to that today and throw in silver as food for thought as an added possibility. To be completely honest, we don’t have an absolute answer for this one; the goal is merely to bring the topic back to the surface for some discussion and thought.

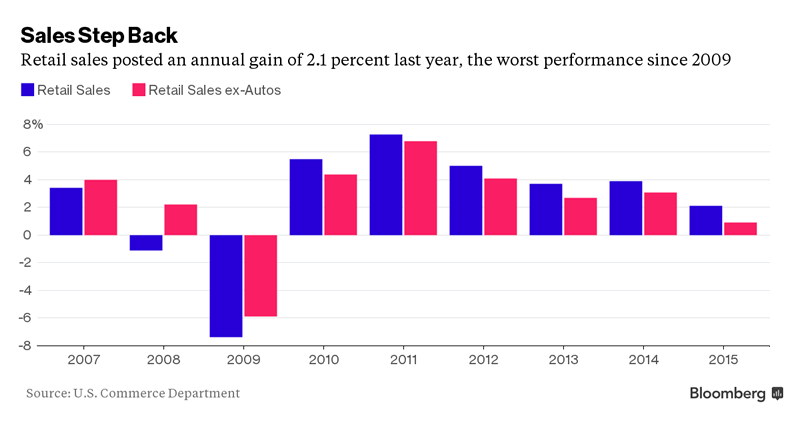

As this piece goes to press so to speak, global stock indexes were creamed as the latest retail sales data in America were released. Shocker of shockers, a disturbing trend is emerging. Of course when you look at China’s slowing manufacturing it makes perfect sense. While America doesn’t consume all of China’s exports as many believe, it is without doubt that the pullback in retail sales (quite a trend – observe the chart below) is contributing to the slowdown in the East.

Again, it is important to note that retail sales data is tabulated in dollars, not units. So the cost of gasoline dropping results in lower sales just as when gasoline goes up in price, that pushes retail sales higher, all else equal. Notable in the report was a 1% drop in spending at general merchandise stores. Prices at the consumer level ex-fuel haven’t dropped that much, which portends stagnant demand. 6 of the 13 major categories covered by the Commerce Department in its calculation of retail sales were negative.

Possibly the most humorous portion of the analysis seen regarding this latest disaster-plagued report was the wonderment of yet another establishment stooge economist who stated that the labor market is in ‘excellent shape’ so the retail sales data must be incorrect or skewed. So for the last four years or so, the labor market has been improving thanks to the bureaucrats at the Department of Labor and their creative modeling, yet spending is dropping and consumers are STILL accumulating debt. Anybody who thinks they can explain that away, please step to the front of the line.

Theme #2 – Monetary Velocity (Or Lack Thereof)

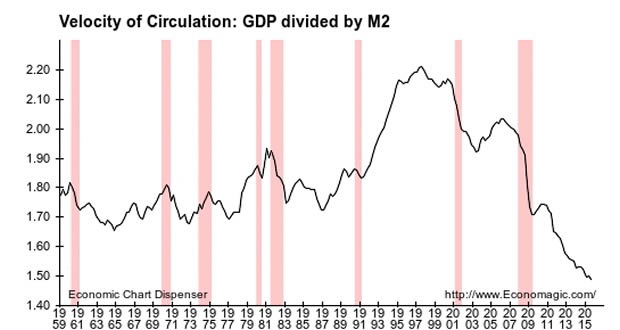

The next theme is something we’ve been following for quite some time as well and that is the continued slowdown in monetary velocity. The chart below paints an ugly picture. Notice that while all areas where velocity is contracting are deemed recessionary by the economic ‘authorities’, every single acknowledged recession since 1959 occurred during a period where velocity was contracting. Every single one.

As you can easily observe from the chart, monetary velocity has never been lower than it is right now. According to Wikipedia:

“The velocity of money (also called the velocity of circulation of money) refers to how fast money passes from one holder to the next. It can refer to the income velocity of money, which is the frequency at which the average unit of currency is used to purchase newly domestically produced goods and services within a given time period. In other words, it is the number of times one dollar is spent to buy goods and services per unit of time.”

So what we can infer from the qualitative chart and the definition is that one dollar is being used fewer times to purchase items per unit of time than during any other period since tracking of the metric began in 1959.

What this doesn’t mean: it doesn’t mean there are fewer dollars. There is no way to derive the overall financial health of individuals from this data. What we can infer though are some possible reasons why money might be moving in a rather sluggish fashion around the economy. It is possible (and very likely) that inflation has created a situation whereby GDP rises, but the number of transactions in a given period remains relatively constant or lags the expansion of GDP. As prices increase (regardless of the reason), the number of transactions in an economy will be constrained by the supply of money available. Put another way, when the rate of price inflation exceeds the rate of monetary inflation, the number of transactions will be constrained to at least some degree and hence velocity of circulation will drop. While price inflation is a function of monetary inflation and NOT the reverse, it is possible to have periods of time where price inflation exceeds monetary inflation due to exogenous factors such as shortages, price controls, and other insults to general equilibrium.

Another possibility is that the US really has a very high savings rate and dollars are in bank accounts versus ‘out in the economy’ participating in transactions. While many might scoff at this notion, banks have very recently stated that they are FLUSH with deposits. Again, we must remember that we are talking about the aggregate here and personal experience – or even the experience of most – can vary greatly from the aggregate simply because it doesn’t take much to skew the results. For example, you can have 99 families just scraping by with little or no savings and one billionaire who has most of his money in a bank. So in the aggregate, the bank is flush with nearly a billion in deposits, but that isn’t the experience of most of the group.

Still another possibility is that purchases are postponed until the money for those purchases can be saved, although the data doesn’t support this phenomenon on a meaningful scale. Likely, the reason for tanking monetary velocity is some combination of all the above factors, plus possibly some others not stated here in the interests of brevity.

What does it really mean though? What would be instructive is if were possible to reconstruct monetary velocity back to 1900 – when the country was still on a gold standard. That would create a somewhat honest baseline from which further examination could be performed. Even without the benefit of such data, however, we can properly deduct that in conditions where the savings rate is very low for most individuals and the various types of consumer debt continue to grow that declining velocity of circulation is indicative of economic malaise.

Theme #3 – Interest Rates

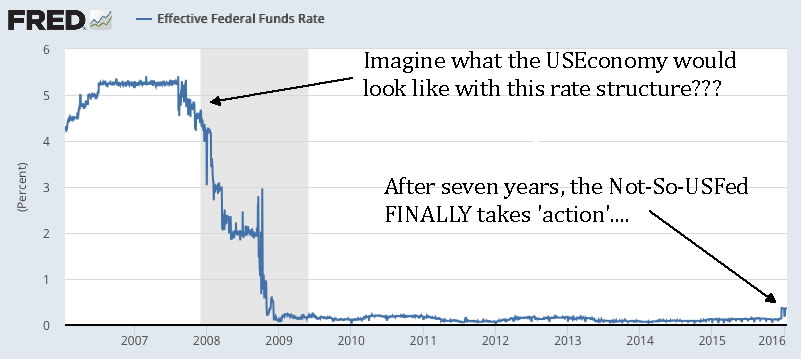

Possibly the biggest economic news of 2015 was the quarter point rate hike the not-so-USFed imposed at its December meeting. While in the grand scheme of things a quarter point means very little, it didn’t take the banks long to raise their prime rates a corresponding amount and stick the knife a little deeper into a country already in hock beyond comprehension. It is disgraceful to hear public officials in America talk about ‘borrowing from our children’ to continue the trend of big government. America has already borrowed all its children’s money. And its grandchildren’s money for that matter.

Buried but not hidden in the US central bank’s release after its last meeting was the notion of 4 more quarter point hikes in 2016. These will no doubt be passed along to the borrowing public, while the saving public will see little if anything in the way of benefits and will no doubt be treated to more fees, service charges, and penalties by the banks for various transgressions such as not maintaining a certain minimum balance.

Pretty much everyone is willing to admit that America, along with most of the West, is hooked on debt. This addiction is displayed at every level, whether it is a township, a county, a province, the consumer, states, or national governments. For much of the past decade, all of the above enjoyed relatively low interest rates on their binge borrowing. Some of borrowing became necessary thanks to price inflation outstripping wage growth. Much of it was foolish. Regardless, the addicts are now going to pay the price as rates increase. The not-so-USFed knows this of course; it was part of the plan. ‘Stimulate’ the economy with below equilibrium rates, get people further in debt, and then stick it to them.

It is also worth noting that various not-so-USFed ‘officials’ have been quickly jumping the proverbial ship on the continuation of raising rates ‘if the economy slows down’. NY Fed President and CEO William Dudley said he would even consider negative rates. Note that Dudley is the President and CEO of the NYFed. We couldn’t help taking a jab at those poor tenured economists/drama queens who continue to insist the not-so-USFed is actually a branch of the US Government. All that aside, the interest rate futures markets now place the odds of a January rate cut back to near zero at 10% and rising. After 1/15/2016’s horrendous retail sales report, that probability is sure to climb. The same futures market data points to the next possible rate hike being October 2016 (if ever).

What most folks don’t understand is that the proverbial fallout rolls downhill. National and municipal governments simply pass the buck – pun intended – and raise taxes, fees, and levies to offset their increased borrowing costs. The guy at the bottom of this perverse pile is the one who is going to hurt the most – even if he didn’t partake in the foolishness. It is a precise case of espousing capitalism when times are good, then socializing the losses so to speak when it all goes south.

In summary, the three themes examined above continue to develop as expected with the possible exception of peak oil. There are too many unknowns to say with any kind of certainty what is going on there. Oil melds with the currency markets, geopolitics, and is a power tool of global influence. One thing we can be sure of is there is a limited supply available – even if it is a hundred years worth. At some point there will either be a transition away from oil to another energy source or there will be a mad scramble as the brick wall approaches. Judging from past performance, the latter is a safe bet.

2016 has gotten off to a poor start economically and financially and there exist sufficient pressure points to make for a very mediocre year and that is a ‘best case’ type of scenario. We aren’t partakers in the sudden overnight crash thesis – the globe has been crashing in slow to medium motion for nearly a decade now and it remains in the establishment’s best interest to make their moves in an orderly fashion. 2016 more than ever is a year you need to be your own advocate. If you’re already doing that - fantastic. If not, you need to get busy; there is much to be done.

You can sign up to receive updates on this situation as well as other ‘My Two Cents’ articles by clicking here. Your email is kept strictly confidential is not shared, sold, or otherwise disseminated.

By Andy Suttonhttp://www.my2centsonline.com

Andy Sutton holds a MBA with Honors in Economics from Moravian College and is a member of Omicron Delta Epsilon International Honor Society in Economics. His firm, Sutton & Associates, LLC currently provides financial planning services to a growing book of clients using a conservative approach aimed at accumulating high quality, income producing assets while providing protection against a falling dollar. For more information visit www.suttonfinance.net

Andy Sutton Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.