Market Decline Will Lead To Pension Collapse, USD Devaluation, And NWO

Stock-Markets / Financial Markets 2019 Sep 10, 2019 - 05:07 PM GMTBy: Raymond_Matison

It is the goal of this article to project the current financial, economic, and geopolitical trends to a logical and credible future outcome. Some of these trends such as in demographics have been in motion for decades, while other trends such as those for negative interest rates have been developing for a much shorter time frame. Pension asset accumulation and eventual payout also extend over decades, and therefore are reasonably predictable. Even money and credit creation trends by the FED have been in place for a long period of time. Finally, the extended bubble market in fixed income and equities, in light of slowing economic trends, provides some assurance to future price expectations.

It is the goal of this article to project the current financial, economic, and geopolitical trends to a logical and credible future outcome. Some of these trends such as in demographics have been in motion for decades, while other trends such as those for negative interest rates have been developing for a much shorter time frame. Pension asset accumulation and eventual payout also extend over decades, and therefore are reasonably predictable. Even money and credit creation trends by the FED have been in place for a long period of time. Finally, the extended bubble market in fixed income and equities, in light of slowing economic trends, provides some assurance to future price expectations.

It is anticipated that a market decline in global economic activity will reduce fixed income and equity prices such that it will start an unvirtuous cycle between the consumer as driver to the economy and financial markets. Market declines will become noticeable by negatively affecting pension asset accounts and actual payouts. Demographic trends will frustrate maintaining our Social Security viable, and severe measures will need to be taken. State, municipal, teacher, corporate and individual pensions are already falling short of their promises. The FED has a publicized goal of increasing inflation, while the President wants a weaker dollar. They will both succeed. By the time that we exit from the coming Great Global Recession, our dollar very likely will no longer be the world’s leading reserve currency, which will result in a dramatic decline in the purchasing power of the dollar affecting negatively domestic and foreign dollar asset holders, or those receiving pensions in dollars. The world will have become financially and geopolitically multipolar resulting in a new world order.

The anticipated events in this article are more than concerning, they are outright frightening! However, you must know that this former major Wall St. firm investment banker now decades later as forecaster-author is trying not to present a false, negative outlook. Accordingly, these forecasts and opinions which, while cataclysmic, are intended to be realistic rather than negative. These opinions will not be easily accepted by those hoping for a better near-term future, nor those trying to obscure the truth. Cassandra, in Greek mythology a woman who was gifted by the god Apollo to accurately foresee the future, but cursed such that no one would believe her - is exactly the feeling one gets in making such a dire forecast. This future is here already and will become visible to everyone as it will play our over the next decades.

America’s retirement system components

It is no longer newsworthy to acknowledge that Social Security has a structural funding shortfall and that major additional adjustments will need to be made to increase funding revenue, make significant reductions to benefit levels, or increase the qualifying age to begin receiving benefits - just to keep the system solvent a few years longer. Suffice it to say that one part of the nation’s total pension system for citizens is not in doubt regarding its long-term sustainability – it cannot be maintained in its present form. Its $16 trillion unfunded liability is simply too large to fund. So benefits will need to be cut- a fact acknowledged by Social Security’s own management. These cuts, when compounded by purchasing power loss due to the FED seeking to accelerate inflation and loss in the dollar’s value due to its receding from the global reserve currency will result in significant reduction of real income to pensioners.

Driving this inequality between funding and benefits disbursed is the rapid growth of retirees largely stemming from the explosion of births and subsequent population growth following the end of WWII. Our victorious GIs came home, formed families and had children. Now that bulge in population growth has been retiring putting stress on funding these retirement benefits.

The original Social Security system was not intended to provide complete retirement for citizens. According to President Roosevelt, it was to “give some measure of protection to the average citizen … against poverty-ridden old age”. Thanks to politician’s often promising additional benefits for election purposes, over decades it eventually evolved into a worker and employer paid-for benefit on which a large portion of the populace soon depended entirely.

Once cost of living adjustments (COLA) due to inflation were included in 1975 to increase Social Security benefits, it became plausible that Social Security could serve and provide a near adequate level of retirement income to a large segment of the population over their lifetime. The problem of this benefit system was that it was funded by payroll deductions and therefore dependent on the balance between the number of people working and funding payments, and the number of people receiving benefits. At present there are about 128 million full-time workers paying 6.2% of their earnings up to $132,900 of income, with contributions matched by their employers as funding revenues into the Social Security Trust Fund.

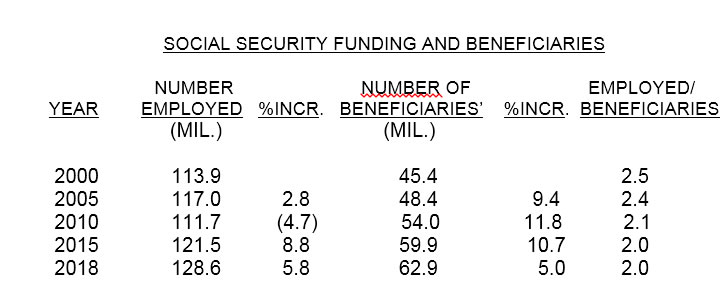

Until their own retirement, these post WWII baby boomers were employed for decades, thereby contributing to the funding of this seemingly sustainable system. The following table shows the number full-time employed by year, that is, those contributing to the Trust Fund. A far larger number of employed released by the Bureau of Labor (158 million) includes part-time, seasonal, farm, and others whose contribution to the S.S. Fund is limited. This table also shows the number of people receiving old age retirement benefits. Note that the number of those retired is growing at a rate several times that of the number increasing as employed - demonstrating the growing disparity between the rate of growth in the number funding contributors to the system when compared to the number growing who collect benefits.

What this table also demonstrates is that between the year 2000 and 2018 the number contributing to the SS Trust Fund increased by 14.7 million persons, but the number receiving benefits increased by 17.5 million – a not sustainable trend. This table also shows the declining number of people supporting each person receiving benefits – another trend that is not sustainable. According to Social Security’s actuaries “The program was stable when there were more than 3 workers per beneficiary. However, future projections indicate that the ratio will continue to fall from two workers to one, at which point the program in its current structure becomes financially unsustainable.”

The amount paid into the fund in 2018 was $831 billion, while the amount paid out was $853 billion, demonstrating that cash flow of the Social Security system has already turned negative. It is projected by their actuaries that by 2034, just fifteen years away, its present $2.9 trillion trust fund will be completely depleted. Social Security is legally permitted to spend more than it takes in only until its trust fund is depleted; thereafter, benefits are limited to what is collected from payroll taxes – signaling a future reduction in benefit payments.

Closely related to Social Security are the generous pension benefits provided for state and municipal government workers, including teachers. These funds have also been evaluated by numerous professionals and judged to be critically underfunded, largely in part due to insufficient contributions driven by local government insatiable spending, budget deficits and growing acknowledgement that many state or municipal governments are failing financially. According to Pew research in 2017: “states had 69% of the assets needed to fully fund their pension liabilities.”

Another major part of our nation’s total pension system is based on corporate pension funds. Corporations concerned exclusively with earnings growth have over decades moved from defined benefit plans to defined contributions leaving employees increasingly at risk of having inadequate retirement assets. Aggressive actuarial assumptions for investment returns lowered contribution levels, and raised risk from lower grade investments. In light of current record low interest rates with added indications now for likely further reductions by the FED – these pension assets will also be inadequate to fund hoped-for retirements.

Due to stock buybacks, which have increased debt and reduced equity, several large bond fund managers have been so concerned about the declining quality of corporate balance sheets that their bond funds avoid corporate debt entirely. Such concern by investment professionals should extend to concern whether corporations will fund pension contributions at adequate levels, and whether their bonds will remain suitable investments for retirement assets.

The remaining component of the total pension system is that which essentially is funded by private insurance purchased by the public. In normal times these should be the most properly funded and secure retirement benefits. However, we are not experiencing a normal economic environment, nor do we have properly functioning financial markets. The rapid decline of, and record low bond yields endanger the entire insurance industry which by law limits their choice of investing. The overall return on investments for the life insurance industry in 2017 for its general account was just 4.3%. Group annuities held in Separate Accounts allow a greater share of assets to be invested in equities, which increases both potential return and risk.

Reviewing these four separate areas of retirement sources suggests that all of them are in danger of not fulfilling their intended obligations to society. Noteworthy is the fact that none of the present funding shortfalls takes into account our bubble financial markets or the high probability of a coming recession, or worse. Therefore, any market decline in our fixed income and equity markets would increase this shortfall by significant amounts. For example, making the reasonable ballpark assumption that overall pension funds are funded at 60% (with significant individual variances), adjusting for just a 33% decline in financial markets would reduce the presently underfunded plans of 40% to a level of being underfunded by 60%. Such a compounded level of underfunding is unlikely to be recovered during a time of multi-year economic and financial duress, and appears ominous for America’s present pensioners, and those hoping soon to retire. So what happens to pensions if markets decline by 90% as happened in the 1930s depression, which also took decades to recover?

Does this scenario describe the totality of pensioner exposure to calamity? Unfortunately not. With global economies slowing and financial markets already heading lower there is the real likelihood of our dollar losing a noticeable portion of its purchasing power! This is the risk associated with the dollar losing its dominant global reserve status. The compound effect of present underfunding, market decline, targeted increases to inflation by the FED, and loss of our global dollar purchasing value would destroy pensions for everyone, likely resulting in reviving the old colonial custom of tar and feathering – in this case our politicians, bankers, and responsible elites.

According to Wikipedia, “tarring and featheringis a form of public torture and humiliation used to enforce unofficial justice or revenge. It was used in feudal Europe and its colonies in the early modern period, as well as the early American frontier, mostly as a type of mob vengeance.” Of course no vengeance would be adequate for the destruction of pension assets or retired livelihood totaling nearly two hundred million of America’s citizens. So when the public becomes outraged due to their pension implosion and impoverishment, the people will be in open revolt against those believed responsible. Even the militarizing of our police to control the populace will not help, for policemen also have hopes to retire with dignity, and therefore ultimately will not follow the directives of our elites in government.

Major contributing factor to pension collapse

For over a century our Federal Reserve central bank has been a constant companion to our economy. Its founding in 1913 also established the need for individual income taxation. Soon thereafter, the United States chose to participate in WWI, as funding for the war could obtained by selling government bonds which could be paid off from both income taxes or simply by printing the money. It was legal but arguably immoral, since such printing devalued the existing currency value. It is worthwhile to recall Warren Buffet’s comment that “inflation at any amount is theft”. The printing of more money after this war initiated and sustained the “Roaring Twenties”, but when England’s central banker asked its U.S. counterpart to help support England’s currency, the FED raised interest rates in the late 1920s and the market crashed creating the Great Depression.

It was the incredibly huge amounts of military spending for WWII with its attendant exploding government debt, again facilitated by the FED, that with a judicious point of entry in that war - after the European belligerents had bled each other sufficiently, that America entered the war and won the conflict. After the war the FED established the “Bretton Woods” monetary system where the U.S. dollar would become the global currency, with the dollar backed by gold at $35 per ounce.

As our soldiers returned home, pent-up demand for homes, consumer products and a normal life style moved economic growth briskly. As the Korean and Vietnam wars soon followed, our military-industrial complex expanded and more money was printed. As banking technology evolved, vastly more money was created by banks simply extending credit to borrowers.

In the interim, America’s politicians started its Medicare programs, and President Johnson started his “war” against poverty to establish “The Great Society”. The cost of these programs required massive money expansion, such that alert European countries started to demand gold at the “guaranteed” rate of $35 per ounce. Soon the gold window was “temporarily” closed in 1971, and money printing ballooned in subsequent decades as the dollar’s purchasing value continued to plummet.

As a comical and non-economic measure in the loss of the dollar’s purchasing power it is well to recall a popular post-war book printed in 1957 entitled “Europe on $5 a Day”. If this book were to be updated today, what sum would be in its title? This updated title would realistically indicate how much loss of value in the dollar we all have suffered due to the policies of our dominant privately–owned central banking system.

In the 1970s, America’s traditional family came under attack, as the difference between the cost of living and real wages earned diminished the head of household’s ability to provide adequately for his family. This meant that his wife was required to go into the workforce in order to provide for the shortfall of real income. That changed the traditional American family, values and its morality, but it seemed to fill the loss of dollar value income void. As money creation and credit expansion were relentless with attendant loss in the currency’s purchasing power, ultimately even the two family income was insufficient in real terms to provide adequate income relative to ever-rising living costs.

People being rational, understood that if two incomes were hardly sufficient for their families, they would have to control or diminish the size of their families. The cost of bringing in children into this world and educating them simply was becoming too expensive. Thus the rate of births declined, and twenty years later there were fewer adults entering the work force, directly detracting from needed contributions to Social Security, expanding its underfunding. Therefore, present inadequate Social Security funding can be viewed as a direct consequence of central banking money and credit expansion policies, and its attendant effect on inflation and loss in purchasing value of the dollar, smaller families, and a decelerating economy.

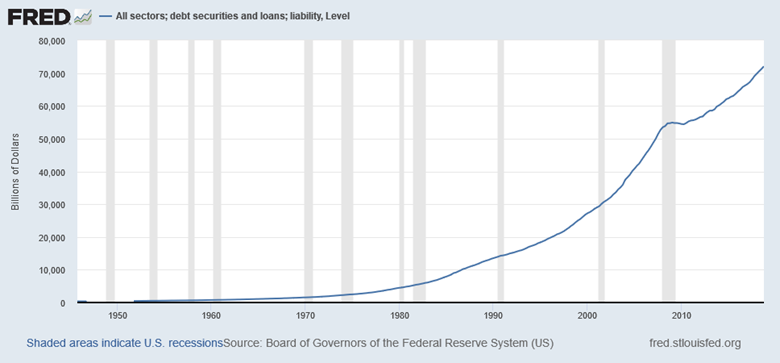

From the 1960s, easy credit conditions were extant to facilitate expansion of credit for government, corporations, and consumers. The following chart, which looks deceivingly simple, shows the dramatic expansion of credit created money. Credit growth exploded from $1 trillion in 1965 to over $72 trillion currently – an astounding 8.2% annual rate of expansion over the period, and a 5.6% rate since the year 2000.

Continuing purchasing power loss of the dollar forced these reduced-size two adult working families to resort to borrowing against their home equity – with predictable results. As the public borrowed to their limit and beyond, the expected result of a financial crash followed. The central bank then responded by creating trillions of additional new dollars, “saving” our banks and economy, and financial markets. The FED’s monetary and credit expansion policy reducing purchasing value of the dollar was now causing borrowers to invade their home equity thereby creating civilian debt slaves. The original 1913 dollar now had the purchasing power of 3-4 cents.

The world is now facing record low and negative interest rates. Negative interest rates, what does this mean? It means that our manipulated central bank financial system is desperate and falling apart. Please note that negative interest rates in a free market are impossible! You will not pay me for me to borrow your money, and I will not pay you to lend you mine. No independent lender will fall for this ruse. Negative interest rates can only occur in a totally controlled and manipulated environment by an organization which has the power to impose negative interest rates on world markets. That is the world of incessant money printing, and debt and credit expansion through private-ownership central banking. However, be prepared that continued expansion of debt and money supply, financial repression, and negative interest rates are a precursor to currency collapse and hyperinflation.

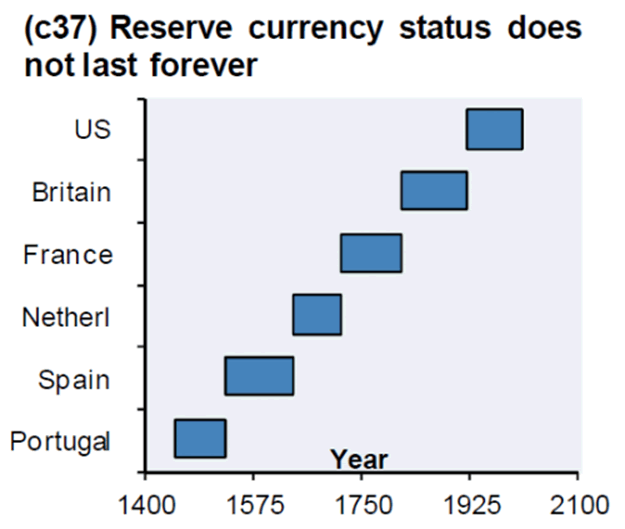

Historically, the time for any one country’s global dominance and its currency has been limited. This now well-recognized and often seen chart below depicts the time periods in history during which a country and its currency ruled the globe.

This now oft-cited chart needs to be updated to include the next iteration. But rather than showing countries on the Y-axis we should show currencies, because it is hoped that in the near future, with multi-polar power sharing, there will be multiple different global currencies rather than just one, and could include a currency which is not owned by a nation state.

We have finally entered the edge of a financial quagmire, a century in the making, that neither government, capitalism, socialism, not even the central global banking system itself can repair. We are not confronting the mortgage, stock or the bond bubble, we are facing “the everything” (including the fiat dollar) bubble. Accordingly, it is not that these markets will crash, it is that the very monetary system will now change from its dollar denominated global currency to the next several contenders.

Judicious propaganda to which we have been exposed to may have made it seem that wisdom of the FED’s policies improved America’s economy and the lives of its citizens. In reality, it was the constant and unrelenting advance of science and technology that produced products and services previously unimagined that benefited lives and provided tangible improvements. Rapid increase in credit and money has unfortunately kept millions of Americans from adequate savings accumulation and retirement income, and supported military adventurism with its destructive and deadly aftermath, with still to come possibly cataclysmic international consequences.

Dethroning the unipolar dollar

As the world slides into the next recession, the U.S. will be a participant – it cannot escape. This will have a multiyear effect in degrading our pensions and living standards, as discussed previously. By the time the world exits from this recession, which will take a half a dozen years and likely more, the transition will include the dethroning of our dollar from its global preeminence, and the creation of a new world financial and geopolitical order.

At a recent meeting of bankers this year, Mr. Mark Carney governor of the Bank of England observed that “the USD has had a destabilizing effect in the world as a reserve currency” and that a “Synthetic Hegemonic Currency” could replace it. His specific example for such a replacement currency mentioned Facebook’s Libra. One must admire Mr. Carney’s steadfast loyalty to the central banking establishment. His comments do confirm that the present system has not been working, but has been destabilizing. In fact the system has been destroying the value of the dollar for decades, diminishing savings and the income on it, changing the foundation of the American family and its very culture, enriching the already wealthy with asset bubbles while impoverishing everyone else, destroying people’s pensions while creating credit-based debt slaves, and supporting military aggression and destruction worldwide. Destabilizing? How deliciously insightful, Mr. Carney! Yet Mr. Carney is asking the world to continue accepting its central banking rule, as it proposes to substitute an even more fully centrally controlled, new cashless electronic global system for the fiat money central banking failure. That is real hubris.

What the world needs is currency decentralization so that one failing system does not take down the world. It needs decentralization so that one cabal does not control our global population. The world contains more than seven billion people, with nine different civilizations and hundreds if not thousands of distinct, varied cultures – and each has their leaders and ruling establishments. There will always be a ruling class in each country, but there is no benefit to humanity from one group ruling the world. For years liberals have been promoting the idea of diversity - in the instance of money emission, diversity is good.

A cashless electronic system would be at a huge risk of cyber-attacks and break-ins since the prize would be beyond comprehension. Most internet providers have already experienced compromise affecting hundreds of millions of their accounts. Equifax, the credit rating company had 144 million records compromised and stolen – so what could possibly go wrong if all your money and assets, together with everyone else’s on the planet was stored on line and controlled by one system?

The dollar has been the global reserve currency since the founding of the Bretton Woods gold-backed dollar system. In a short twenty years the U.S. had breached its agreement in printing more dollars that its store of gold valued at $35 an ounce supported. A few years later it breached its international agreement to exchange dollars for gold and closed the gold exchange window. Free to print as many dollars as needed without a gold constraint, the world was soon flooded with dollars. If the dollar was to become the global reserve currency, enough dollars needed to be created so as to satisfy universal demand. The logical implications were that the U.S. would need to run budget deficits, become a creditor nation in order to satisfy global demand for dollars by issuing Treasury debt and the attendant dollars (the Triffin dilemma). Today that Treasury debt is at a level that servicing it at normal interest rates would destroy our economy and the currency. So the dollar must retreat from its global reserve position.

The top candidate for increased global currency responsibility is the yuan. However, because the yuan is not freely exchangeable in the marketplace, it is not considered ready for this expanded role. Accordingly, various interests have been prodding China to make the yuan freely convertible. The Chinese are too wise, and are not taking the bait. They understand that in these manipulated markets a tsunami of speculative money would flow in to undermine the yuan and its economy – an example that over decades has been experienced by many other countries. So China is likely to make the yuan fully convertible only after America’s dollar weakens sufficiently, and the yuan is not in danger of being swamped by speculative flows. Cautiously, over time yuan’s role in global finance will increase. See: Currency War Combatant Capability Comparisons: http://www.marketoracle.co.uk/Article64054.html

Another potential candidate for a global reserve currency is the Euro. However, its recent multitude of internal bickering among member states, and apparent unwillingness by some members to give up their sovereignty completely to unelected rulers at the EU suggests that the European Union as it exists today could unravel, or at a minimum have dramatic changes in its membership roster. In addition, its preponderance of negative interest rates will play a more dramatic effect on European pensions and economy than that in the United States. Add to this the announcement that Germany, its financially strongest member, is slipping into a recession while its two largest and most powerful banks are at the precipice of financial doom does not bode well for the Euro expanding its role.

Europe has been dominated by U.S. free trade, the dollar, and its military might for seven decades. Opportunities for Europe to increase trade eastward or join China’s Belt and Road Initiative have been discouraged by the U.S. calling forth various sanctions. However, Europeans understand that their brighter future now faces east not west. Indeed, increased trade from the mid and far east in the future may save the Euro from calamity and over time strengthen it to become one of the effective and strong global currencies. This awareness and gradual relative disengagement from the west to the east unfortunately also has negative implications for America’s global currency, and its effect on American livelihood. Another candidate for global currency is the SDR, which would be issued by the IMF to its global membership countries. This currency already exists in a limited amount, and if participating countries agreed, it would be effective in global trade among countries. The SDR would be an attractive solution to America in that the dollar is a major component of this currency, and the IMF historically has been controlled by the U.S. By virtue of it being the only country holding more than 15% of the voting shares, and any major change to the IMF Agreement requiring an 85% voting majority, the U.S. holds veto power. For this reason the SDR as currently structured may not be acceptable to the new global currency contenders.

Bitcoin has exited the imagination of people not wanting to use money controlled by central banks, governments, and those who believe that their financial activities have the right to be private. As several hackers have gained access to exchanges and absconded with investor money from various accounts, the current security of Bitcoin still appears to need improvement. In addition, government has proven access to account information, while demanding taxes on trading profits, diminishing interest in its use from some potential users in the U.S. Finally, institutional central banking will cause laws to be enacted that will try to stifle any system of money that is not under its control. If, however, Bitcoin’s future improved security can be demonstrated to be foolproof, and usage truly anonymous, the world including America will enthusiastically embrace it.

Mr. Ray Dalio, super-capitalist and manager of America’s largest hedge fund Bridgewater Associates, recently released a thoughtful article stating that “capitalism is broken”. Mr. Carney has stated that the dollar is “destabilizing” and will need to be replaced. We must listen carefully to the very important message these globally influential leaders convey, and understand what will be the consequence of their comments or policies.

The world is at a point of financial discontinuity, as new global currencies will compete to gain relevance to replace the dollar. Global equities and fixed income markets will have been in substantial decline affecting retirements and financial security of millions. Negative and record low interest rates will have evaporated interest income on savings, while debt and credit continue expanding to enable individuals, corporations, and government. Being dethroned as the dominant global reserve currency the dollar will lose purchasing value creating unimaginable hardships to Americans countrywide. There will be little consolation to know that the people of Europe and the rest of the world are also suffering. Knowledge for constructing a more just monetary system exists – it just needs the goodwill to be implemented.

Raymond Matison

Mr. Matison was an Institutional Investor magazine top ten financial analyst of the insurance industry, founded Kidder Peabody’s investment banking activities in the insurance industry, and was a Director, Investment Banking in Merrill Lynch Capital Markets. He can be e-mailed at rmatison@msn.com

Copyright © 2019 Raymond Matison - All Rights Reserved

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilizing methods believed to be reliable, but we cannot accept responsibility for any losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors.

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.