SNP-Syriza Labour Coalition Government Election Catastrophe, Debt Binge Before Breakup

ElectionOracle / UK General Election Feb 16, 2015 - 06:51 PM GMTBy: Nadeem_Walayat

Last September the UK had a close call with catastrophe as the tunnel vision SNP failed in their efforts for UK disintegration that would have resulted in a catastrophic breakup of Britain and far worse for Scotland that would literally have started to unravel politically, economically and socially as Scotland itself would soon start to disintegrate as I warned in the run up to the referendum vote. Of course Scotland voted NO, for most Scots are not insane, though succeeded in having the fools in Westminister conned into making promises to increase the annual bribe to Scotland from mostly English tax payers.

Last September the UK had a close call with catastrophe as the tunnel vision SNP failed in their efforts for UK disintegration that would have resulted in a catastrophic breakup of Britain and far worse for Scotland that would literally have started to unravel politically, economically and socially as Scotland itself would soon start to disintegrate as I warned in the run up to the referendum vote. Of course Scotland voted NO, for most Scots are not insane, though succeeded in having the fools in Westminister conned into making promises to increase the annual bribe to Scotland from mostly English tax payers.

I wrote at length in the run up to the referendum that in reality the referendum was NEVER a close call as excerpted below -

18 Sep 2014 - Scottish Independence Referendum Result NO 55%, YES 45% - Vote Forecast

Today approx 9% of the British electorate will turn out to vote on whether the United Kingdom is to be dissolved, of which approx marginally more than half will decide the outcome of the Scottish Independence / Separation referendum. However, whilst the latest opinion polls continue to paint a picture of a too close to call outcome as they oscillate in a tight band of between 48% and 52% for either YES or NO depending on which individual poll one looks at, instead my consistent view has remained unchanged since the start of this year that Scotland will overwhelmingly vote NO, and that the probability for such an outcome remains at a high 70%.

Answering Why the Opinion Polls YES / NO Are So Close

So why such a huge difference between a highly probable NO vote and the opinion polls that are flittering between either outcome. For the answer we need to look at what started to change from late August that has resulted in such a tightening of the opinion polls.

The SNP not surprising state that the tightening in the polls is as a result of as many as 1 million new voters joining the electoral roll who predominantly back the YES cause tipping the polls in the SNP's favour.

However the truth is one of an increasingly threatening nationalist campaign of vandalism, bullying and intimidation of NO supporters who fearful of being shouted down have become subdued in expressing their opinions to others, the silent majority.

As an example a survey by YouGov found that 46% of NO supporters felt personally threatened by the YES campaign, and 49% of NO voters had not always felt able to speak about their views on the referendum.

Therefore the most probable outcome is inline with the polling ranges of before the YES campaigns intimidation and fear phase began to play a prominent role in the frenzy of campaigning of September that rather than a 50/50 tight race is more probably going to result in at least a 55% NO vote victory, and I would not be surprised if the NO vote even breaks above 60%!

SNP-Syriza Bankrupting Britain All the Way to Independence

However, Britain's SNP Syriza-esk party are not done with the UK for their latest baldrick-esk cunning plan is to go into an unofficial Coalition with a Labour government by means of Syriza style taking as many as 30 of Labour's Scottish seats bringing their total to about 35 out of 59 and and thus ensuring that Labour in May 2015 would have zero chance of securing an outright election victory and probably even failing to become the largest party.

The SNP following the script of their euro-zone Syriza brethren will take their scottish majority to hold a minority Labour government to ransom as SNP-Syriza sees the UK purely as a cash cow to milk to the fullest extent possible as illustrated by their publicised agenda to ramp up UK government borrowing by an EXTRA £180 billion as illustrated by demands being made by the SNP leader, Nicola Sturgeon.

“I would certainly hope if there was a Labour government and it was dependent on SNP support - which is the most popular preferred outcome of people in Scotland - then I would hope we could persuade and influence a Labour government to take a more moderate approach to deficit reduction.”

“Debt and deficit would still be falling as a percentage of GDP over these years but we would free up something in the region of £180 billion over the UK to invest in growing the economy”.

However, as my warnings in the run up to the last 2010 General election warned that politician promises of debt and borrowing can be taken with a huge lump of salt as the likely outcome would be for one of many times greater level of borrowing, probably exceeding an EXTRA £500 billion, much as the Tories promises of bringing down the deficit and debt never materialised, and so the SNP's real agenda will be to literally suck the financial blood out of the UK before it went bust, disintegrating under the weight of an unserviceable debt mountain and a currency in collapse, primed for a new DEBT FREE Scottish Currency to be released onto the public as the SNP will have ensured that little or no share of UK debt & liabilities would be honoured.

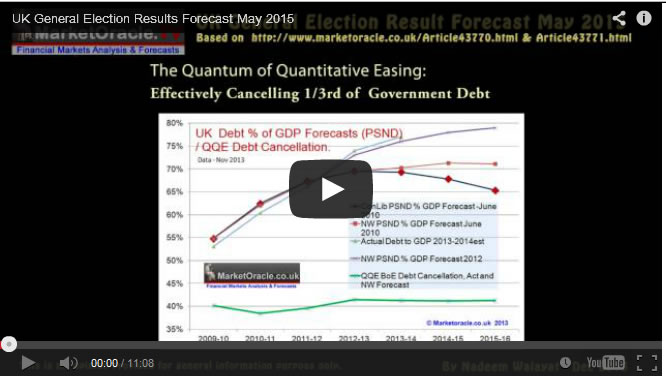

29th June 2010 - UK ConLib Government to Use INFLATION Stealth Tax to Erode Value of Public Debt

Therefore it is difficult to see how the government will be able to achieve its stated budget reduction target of getting the annual deficit down to just £20 billion by 2015-16. Whilst the government is expected to trend close to target for the next 3 years, however thereafter the governments (OFBR) and my deficit forecasts diverge as the coalition governments primary focus will be towards getting re-elected in May 2015. In all likelihood this means that total debt will be over £100 billion higher than that which the government is forecasting as illustrated by the annual budget deficits forecast graph below-

Whilst the ConLib's deficit reduction targets represent an improvement under the Labour governments target that would have resulted in extra borrowing of £478 billion over the next 4 years if the Labour government managed to stick to its targets. However the ConLib government will still expand total debt by £414 billion over the next 4 years, and £471 billion over the next 6 years to reach £1,242 billion, so hardly an earth shattering improvement.

The following updated graph for UK public sector net debt clearly shows that the Coalition government has hit a deficit cutting road block because instead of the deficit falling to around £38 billion for 2014-15, the government will be lucky if the deficit comes in at under £100 billion. Furthermore the trend for persistently high deficits is expected to continue beyond the May 2015 general election as the Coalition government has ramped up deficit spending to buy votes, the net effect of which would be for a total additional debt of over £130 billion beyond the Coalition governments expectations to be added to Britain's debt mountain.

Therefore to imagine a Labour - SNP supported government is going to be able to stick to its debt promises is delusional because the often hyped of economic austerity Con-Dem Coalition are themselves looking set to borrow an extra £130 billion over that which they promised they would. Which means the £180 billion of extra SNP led borrowing could easily double to £360 billion of EXRA borrowing which implies that the current debt total of £1.5 trillion could easily soar to £2.5 trillion by the end of the next parliament, double the £500 billion of Coalition debt added to Britain's debt mountain that makes a mockery of politicians when they make claims that the deficit will be cut and debt repaid.

The only answer / solution that all governments have remains one of stealth default by means of high real inflation hence the Inflation Mega-trend. Inflation is a REQUIREMENT for the Debt Based Economy, this is how governments keep putting off the day of reckoning by attempting to inflate the debt away with printed money and then borrowing more money to service the debt interest which is why virtually all money in an economy is debt money that will NEVER be repaid.

When George Osbourne and David Cameron are stating that they are paying down Britain's debt, they are LYING! The same goes for Ed Milliband if he states that he will cut Britain's debt. NO GOVERNMENT DEBT IS BEING REPAID OR WILL EVER BE REPAID! Instead the truth is that the WHOLE of the economic growth (in real terms) since the May 2010 General Election and continuing into the May 2015 General Election will be wholly as a consequence of some £550 billion of additional DEBT. Again this is a very important point to note that ALL of the economic growth of this parliament is DEBT based, ALL of it, including the current election boom, the debt accrued over the 5 year term will equate to total real terms increase in GDP - virtually pound for pound which is why there is a cost of living crisis because printing money (debt) does not increase productivity, all it does is inflate the money supply.

You should realise by now that the constant drivel about the threats and risks of debt deflation are nothing more than propaganda so as to allow policies such as quantitative easing (money printing) to be more palatable to the general population so as to ensure that the Inflation Mega-trend continues, and all that an Labour-SNP pseudo coalition promises is an even greater magnitude to the cost of living crisis for Britains (England's) hard working tax payers as their productive capacity is funneled as election bribes towards Labour - SNP voting regions and the 8 million or so vested interests sat on their lard asses on benefits for life.

SNP and the Economics of the Oil Price Collapse

Those that may still delude themselves that under a socialist banner an SNP Labour government could be workable much as the Lib Dems and Conservatives have turned out to be, need to take into account not only the not so hidden agenda for the disintegration of the United Kingdom but that where economics are concerned the SNP are completely clueless as illustrated by Scotland's largest tax and revenue earning industry, North Sea Oil that is currently in a state of collapse.

Just as spectacular as the collapse in the oil price has been the collapse in the SNP's Economic Baldrick-esk Master Plan for an Independent Scotland that was wholly based on reaping huge rewards from North Sea oil exports where SNP propaganda had convinced many Scots to Vote to effectively commit economic and social suicide by voting Yes in last Septembers referendum that came close to achieving the catastrophe on the basis of propaganda implying upwards of £7 billion in North Sea oil tax revenues that would be raised to finance Scotland's budgetary black hole, which in the fever pitch of the campaign had reached the heights of £11 billion so as to exaggerate the degree to which Scotland could prosper and fill the void left by the withdrawal of the English subsidy that currently amounts to £9 billion per year.

Even the Governor of the Bank of England did not mince his words by warning "the Scottish economy was heading for a “negative shock”.

The problem with SNP economic propaganda is that it was based on a oil price being well NORTH of £100 per barrel, however a sub $50 oil price does not just mean that an Independent Scotland would have made half the forecast tax revenues i.e. £3.5 to £5 billion, instead the reality is that an Independant Scotland would have faced would be near ZERO TAX Revenues as the average break even price for crude oil is $60 a barrel. Additionally IS would have had to bear the costs of the collapse in the oil industry such as job losses and reduction in other indirect taxes.

North Sea oil companies making losses means many closures and job losses and the longer the oil price persists below $70 then not only will there be no future investment but also a literal collapse in Scotland's oil industry the signs for which were illustrated today with BP's announcing 10% Job losses in its North Sea operations. BP also stated that it expected the oil price to remain below $60 for the next THREE YEARS! Which means many small to medium sized oil companies will go out of business over the next year which illustrates the magnetite of the ineptitude of the SNP's campaign for Independence built upon the oil industry as Scotland Voting Yes would already be in a state of economic collapse, bankrupt much as I warned in a series of articles that would happen and worse during the referendum campaign and why Scotland voting Yes would be tantamount to Scotland committing suicide.

So be under no illusion that an inept Milliband government wagged by the SNP tail will be able to do anything other than to plunge from one worsening crisis to the next, probably even worse than Gordon Browns financial collapse, all the way to disintegration of the United Kingdom.

In terms of the consequences for the outcome of the UK General election ensure you are subscribed to my always free newsletter to get this forth coming analysis and election forecast in your email box.

In the meantime see my existing long standing forecast conclusion as of December 2013.

16 Dec 2013 - UK General Election Forecast 2015, Who Will Win, Coalition, Conservative or Labour?

The following graph attempts to fine tune the outcome of the next general election by utilising the more conservative current house prices momentum of 8.5% which has many implications for strategies that political parties may be entertaining to skew the election results in their favour.

The the key implications of the above graph are -

- The window for an outright labour election victory has ended as of July 2013.

- As of writing an election today would result in a Coalition government with a majority of about 40 seats.

- The window of opportunity for a Coalition government ends by mid 2014 after which there is an increasing probability for a Conservative outright majority.

- A May 2015 general election at an average house price inflation rate of 8.5% would result in a Conservative overall majority of about 30 seats. Therefore this is my minimum expectation as I expect UK house prices to start to average 10% per annum from the beginning of 2014.

And also a video version of the analysis and forecast conclusion -

Source and Comments: http://www.marketoracle.co.uk/Article49461.html

By Nadeem Walayat

Copyright © 2005-2015 Marketoracle.co.uk (Market Oracle Ltd). All rights reserved.

Nadeem Walayat has over 25 years experience of trading derivatives, portfolio management and analysing the financial markets, including one of few who both anticipated and Beat the 1987 Crash. Nadeem's forward looking analysis focuses on UK inflation, economy, interest rates and housing market. He is the author of five ebook's in the The Inflation Mega-Trend and Stocks Stealth Bull Market series that can be downloaded for Free.

Nadeem is the Editor of The Market Oracle, a FREE Daily Financial Markets Analysis & Forecasting online publication that presents in-depth analysis from over 1000 experienced analysts on a range of views of the probable direction of the financial markets, thus enabling our readers to arrive at an informed opinion on future market direction. http://www.marketoracle.co.uk

Nadeem is the Editor of The Market Oracle, a FREE Daily Financial Markets Analysis & Forecasting online publication that presents in-depth analysis from over 1000 experienced analysts on a range of views of the probable direction of the financial markets, thus enabling our readers to arrive at an informed opinion on future market direction. http://www.marketoracle.co.uk

Disclaimer: The above is a matter of opinion provided for general information purposes only and is not intended as investment advice. Information and analysis above are derived from sources and utilising methods believed to be reliable, but we cannot accept responsibility for any trading losses you may incur as a result of this analysis. Individuals should consult with their personal financial advisors before engaging in any trading activities.

Nadeem Walayat Archive |

© 2005-2022 http://www.MarketOracle.co.uk - The Market Oracle is a FREE Daily Financial Markets Analysis & Forecasting online publication.